How could stage three tax cuts influence the Melbourne property market?

Recently there has been a lot of chatter about the Morrison Government tax cuts, and in particular, the looming stage three cut. The Albanese government went into the election stating that Labour would support the proposed cuts and so far, Treasurer Jim Chalmers hasn’t indicated that the government feel otherwise.

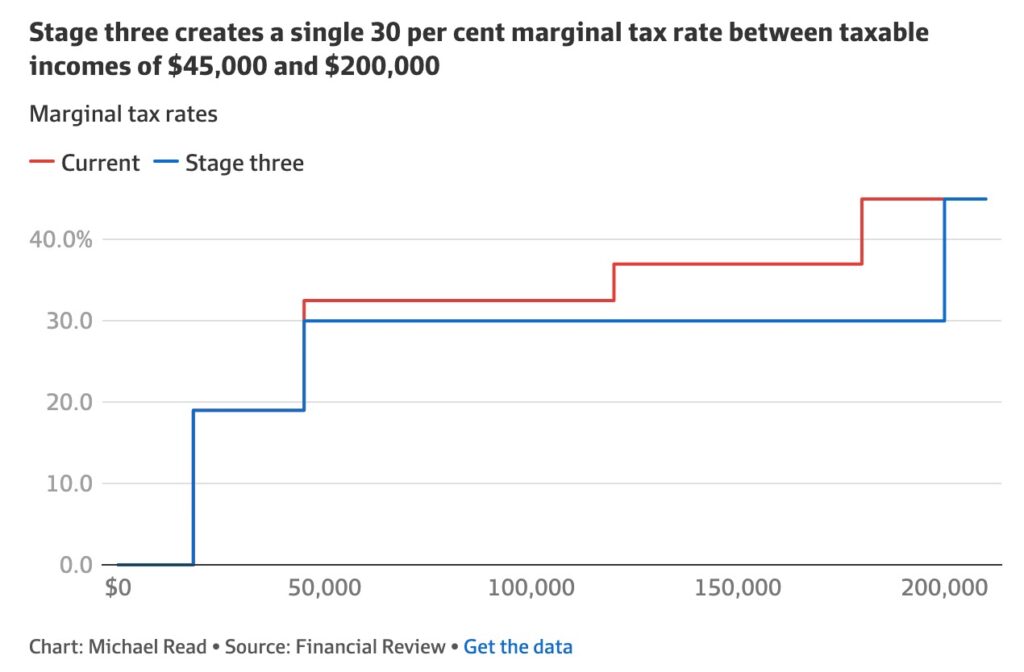

“From July 1, 2024, the 32.5 and the 37 per cent brackets will be rolled into a single 30 per cent bracket, while the threshold for the top 45 per cent tax bracket will increase from $180,000 to $200,000.

Once the changes come into effect, more than 95 per cent of taxpayers will pay a marginal tax rate of 30 per cent or less.” (Source: AFR, Oct 2022)

The following chart shows the proposed removal of two of the current tax rate stages.

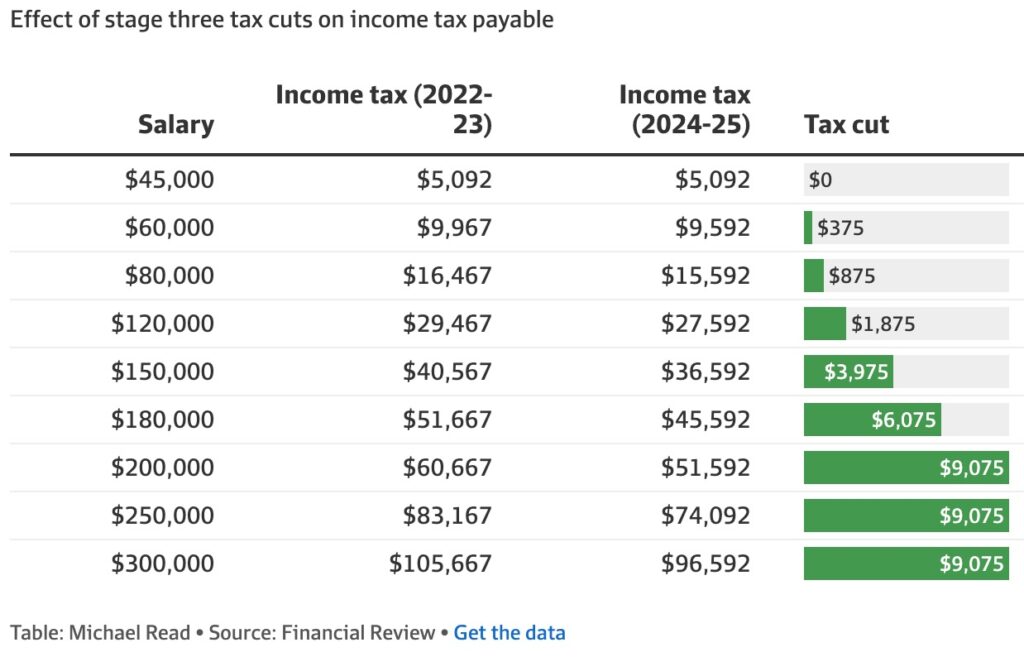

This table below explains the value of the tax cut for each strata of income.

Despite the spirited conversations and opinions about this particular cut, we have to consider how it could impact our property market. Like all cash incentives and net cashflow hikes, markets do get impacted. If we recall the State Government’s COVID emergency stamp duty concession on offer for all purchasers in the sub-million dollar property price bracket, this segment of the market was indeed skewed.

While high income earners, ($200,000 plus) will also reap the benefit of the additional $9,075, it’s not typical for super-high income earners to borrow to their maximum borrowing capacity. Based on my experience with first home buyers and family home buyers, these cohorts are more likely to borrow to their maximum capacity, particularly when buying their first family home.

Broadly speaking, and not taking into account other loan commitments, a rough calculation of a loan representing 30% of an applicant’s income is a reasonable rule of thumb. This indicates that incomes spanning $150,000 to $200,000 could manage monthly loan repayments of $4,167 and $5,000, respectively. Based on 20% deposits, this roughly translates to the $750,000 – $1,000,000 value bracket.

An additional $9,075 per annum of income for a $200,000 income earner(s) reflects an additional $227 per month of loan repayment capacity. This would shift the same borrower’s maximum price point from $1,000,0000 to $1,040,000.

At the $150,000 salary mark, the borrower has an additional $3,975 per year, or $100 per month. By the 30% rule of thumb mentioned above, this represents a smaller shift of $15,000 in buying power. A $750,000 property buyer could increase their spend to $765,000.

While $150,000 salaries are not representative of the average Australian income by any means, it’s in the middle-ring, and gentrifying outer-ring areas that many buyers and household incomes sit in this income band.

And it is the high-earning first home buyers and family buyers who are pushing into the gentrifying suburbs in the quest for a house or family-sized townhouse, (as opposed to an apartment). These are often the most emotionally driven buyers who will push to their spending limit to secure a future family home.

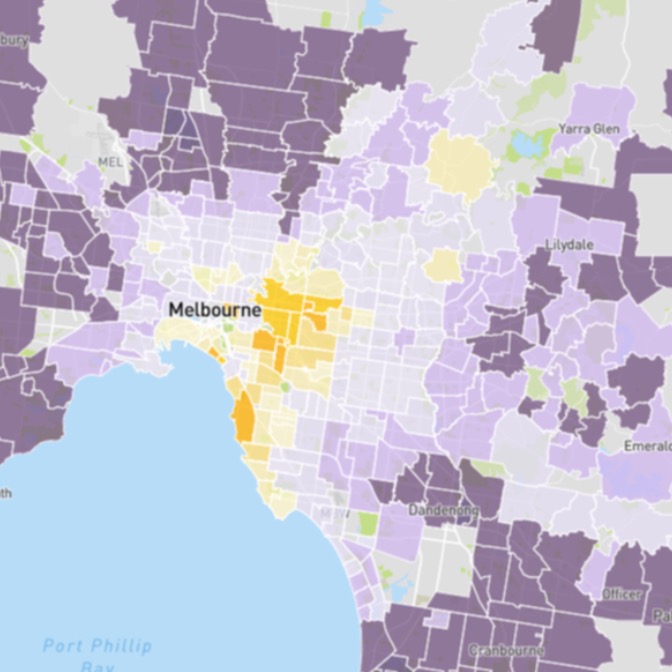

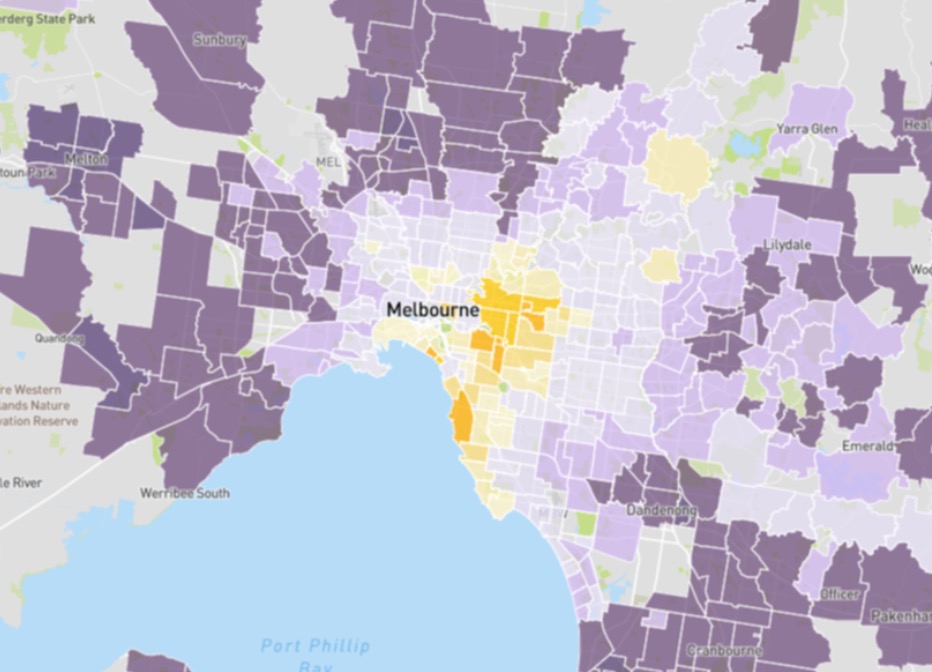

So which areas could be impacted?

I believe that the suburbs in the middle to outer rings as shaded in lavender are the likely areas to experience demand from the emotional contingent who have higher net incomes. These are the buyers who will push their spending from $750,000 to $765,000.

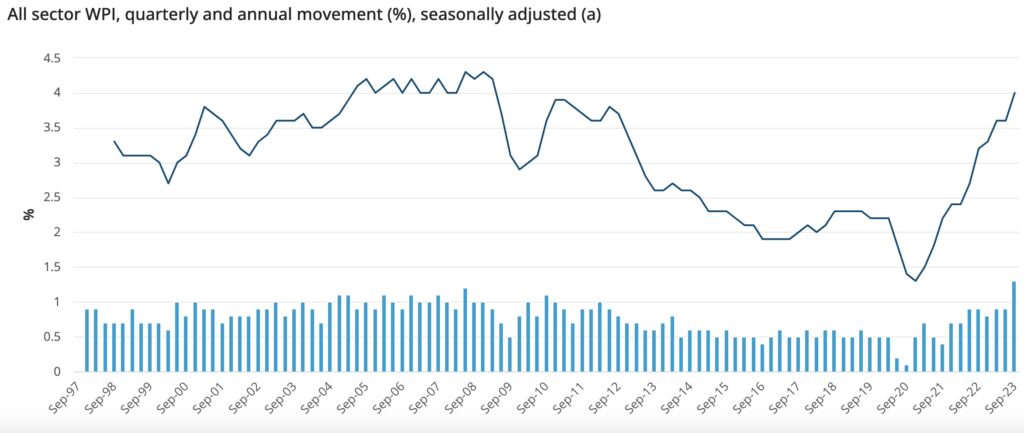

It isn’t only tax cuts that could fuel these markets. Australian wage growth is currently at the highest annual growth rate since the March quarter of 2009.

“The Wage Price Index (WPI) rose 1.3 per cent in September quarter 2023, and 4.0 per cent for the year, according to seasonally adjusted data released today by the Australian Bureau of Statistics (ABS). This is the highest quarterly growth in the 26-year history of the WPI.” (Source: ABS)

2024 no doubt has a lot in store for us all, but it will be intriguing to see how the stage three tax cuts impact our markets.