Land Tax

Nobody likes it. Plenty of investors don’t understand it. There is often some degree of controversy around it, and the rules are quite confusing.

So how do we navigate land tax?

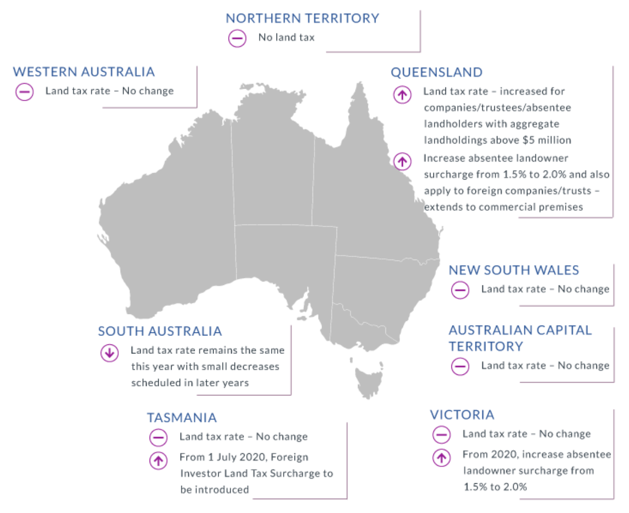

Land tax is a state-based tax, not a federal tax. All of the states have varying tax rates and tax thresholds*, with the Northern Territory being the exception.

NT land owners enjoy zero land tax.

We field all kinds of questions about land tax from our clients, so this article aims to address some of the common questions and point out some of the quirks.

Victorian Land tax is charged individually, and/or with others, (if joint ownership applies) and also to companies and trusts for those who own any of the following in Victoria:

- Investment properties, including residential rental properties.

- Commercial properties such as retail shops, office premises and factories.

- Holiday homes.

- Vacant land

The threshold of $250,000 applies to individuals and ‘joint‘ owners, and the threshold of $25,000 applies to trusts. This figure is based on the land value as set by the State Revenue Office’s appointed valuer.

We often field questions about the appraised value and the accuracy of the valuation, (particularly during a market downturn/correction), and there are avenues that owners can go down if they determine that their land valuation is unfair.

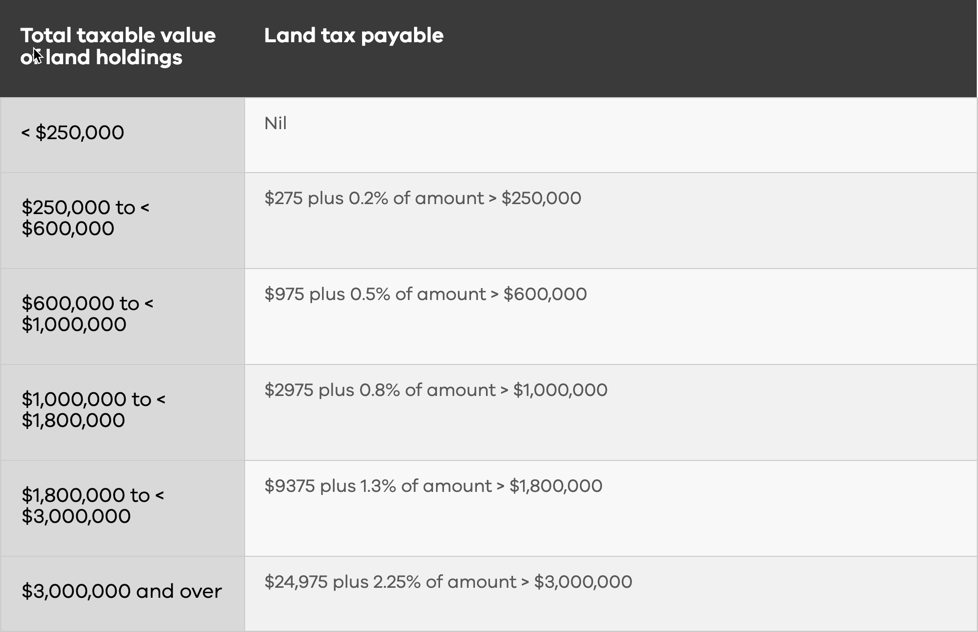

The amount of land tax calculated is based on a sliding scale and is shown here in this table below.

The schedule seems easy enough to understand, but complexity sets in when exemptions, additional taxes and ‘special’ land tax is applied.

A primary place of residence is generally exempt from land tax, but confusion can set in when we consider ‘absenteeism’ and purchases/settlements. In addition, other land can be exempt from this tax including farming (primary production) land, rooming houses, and charitable institutions.

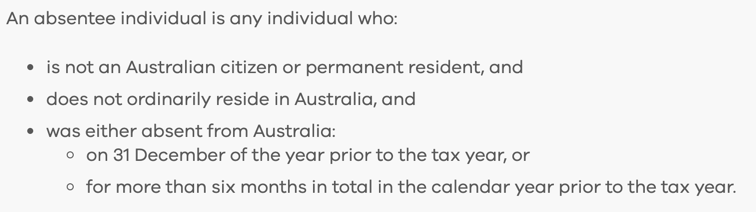

Absentee tax is an additional tax equating to 2% of the land value and this is applied if a land owner is primarily based overseas.

In last year’s state budget, this figure was increased from its former percentage of 1.5%.

Land tax is generally not applicable for primary places of residences, but one of the quirks applies to purchases of property from a vendor who has a land tax obligation against the property they are selling, (ie. the property was held by the seller and the PPOR exemption did not apply). The property may have been sold with a tenancy in place, or it may have been a vacant property, but if the vendor had a land tax obligation for that calendar year, the inbound purchaser would have to pay the pro-rata calculation, regardless of whether it was to be their home or their investment. The two unusual aspects to this tax law are firstly that a home owner is liable for land tax, and secondly, the tax is not calculated for the financial year, but the calendar year.

This seems an unfair piece of tax legislation, but there are ways around it.

In every acquisition we navigate for our clients, we clarify whether land tax is payable, and for owner-occupier clients we endeavour to insert a clause in our contracts that effectively assigns the full year’s tax obligation back onto the vendor.

In situations where our requested clause is rejected, we can also target a particularly late settlement within the calendar year in an effort to reduce our client’s pro rata payment amount. For example, a settlement in mid December will attract 1/24th of the total land tax annual payment.

We are often asked when land tax will be calculated, applied and the tax bill issued. Land tax is calculated as at 31 Dec and typically the tax assessment notice will be sent within the first few months of the year.

It is important to note that any previously ‘missed’ land tax obligations can catch up with owners if the SRO become aware that a property was mistakenly listed as an exempt property.

Payment can be delayed as follows;

One of the most critical questions we field in relation to land tax is the avoidance of it. Many investors consider interstate acquisitions in an attempt to avoid or minimise land tax.

The decision to acquire land in another state should never solely come down to the question of land tax.

If an investor targeted Darwin, for example in an effort to avoid land tax, the lost opportunity and their equity position over the last five years could be far worse than it could have been had they invested in a market that delivered strong growth and applied land tax.

Land tax can indeed be a hefty bill to face, but if the investor’s primary reason for holding that land is for capital growth, they need to consider their cashflow, ability to cover the tax, and the long term financial benefit of owning an outperformance, quality property.

*Source: Chan and Naylor