Managing the cost of the due diligence

One serious burden that buyers face when shopping for a property is the expense of the due diligence. From legal reviews to building inspectors, the costs can really rack up. So many buyers lament the “money going down the drain” when the auction sale result flies past their budget.

We often hear stories about buyers ditching the cost of a building inspection after a couple of failed attempts, only to realise after successfully securing a property that they inherited an expensive issue. And likewise, we have heard stories about buyers proceeding to auction without a legal review in an effort to save a couple of hundred dollars, and later realising that their lender won’t even fund the purchase because they missed a critical title or zoning detail.

We will never let a client sign a purchase contract without a legal review.

We do understand the cost implication of the due diligence and we sympathise when a client misses out at auction after having chalked up some pre-purchase costs.

The importance of the due diligence cannot be underestimated. The potential cost of a mistaken purchase is too great to fathom.

However, this blog aims to help guide buyers to minimise wasted due diligence costs.

It is inspired by a wonderful friend and industry colleague who works as a mortgage broker and assists a lot of first home buyers who really feel the impact of wasted expense.

Following the important pre-approval for finance step, the first and obvious priority a buyer will face after locating a prospective purchase is a legal review. Lawyers and conveyancers are state-based, so in other words, a Victorian contract will need to be reviewed by someone who is licensed to review Victorian contracts. Some legal representatives in other states may hold this license, but typically most don’t. Often the agent will recommend a particular legal representative, but if in doubt, asking friends, colleagues, forums or even a mortgage broker for a referral is a good idea.

The cost of a legal review varies, as does the turn-around time. Some legal representatives offer a certain number of reviews for no charge, but will have the expectation that the purchaser will commit to them once a contract proceeds. Others may have a surcharge in the circa $200-300 range. A large, detailed off-the-plan contract will likely carry a heightened cost, as they can take several hours to review.

First and foremost, there are physical attributes that a buyer can note that could rule out the property. Banks dislike a lot of attributes, ranging from zoning to internal floor area. A buyer can easily eliminate the obvious no-go properties by noting the conditions on their pre-approval letter.

If an apartment or dwelling is above a shop or on a main road, the buyer should carefully check the land data page in the contract for zoning. It is not a guarantee that the property will be commercially zoned, but it is a good possible indicator.

Many lenders will not finance a commercially zoned residence with a residential loan pre-approval.

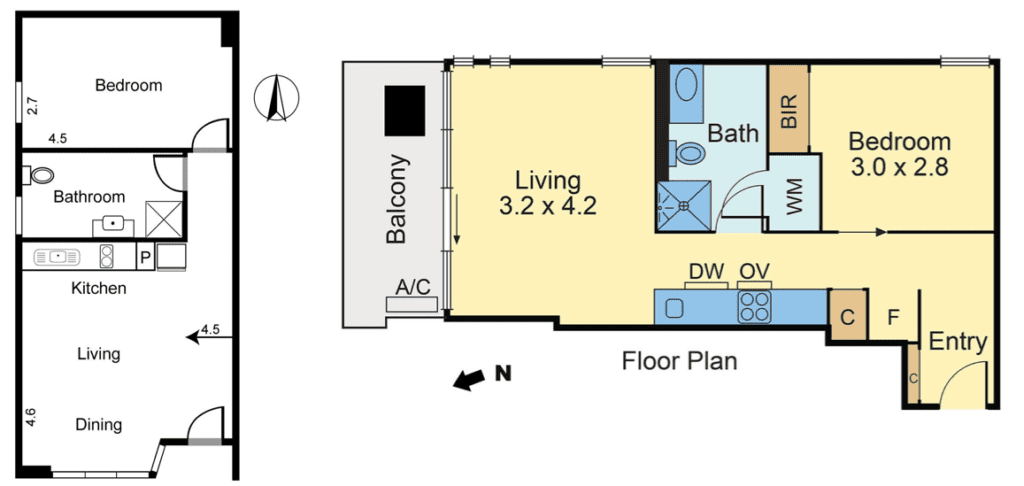

Lenders also dislike small internal floor area apartments. The tolerance levels vary, but it’s safe to work off 50 sqm as a rule of thumb. Agent listings will often display a measurement, but buyers need to be particularly careful that the measurement doesn’t also include balcony, eaves and car park.

53 sqm can easily become 45 sqm once a valuer strips out the inclusions.

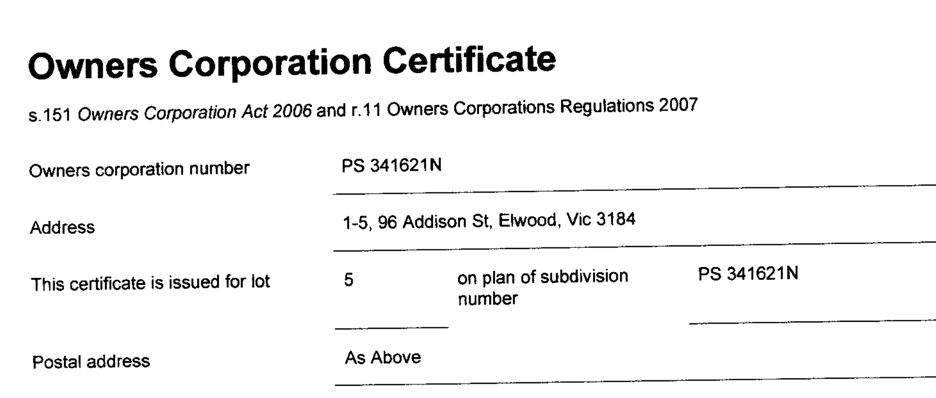

There are also other elements in a contract that could easily rule out a property. These elements are reasonably easy to spot. The significant deal-breaker relates to owners corporation fees and special levies. All a buyer has to do is flick towards the back of a contract to review the Owners Corporation Certificate and AGM minutes.

Once the property has been scrutinised for lender-related risk and ongoing cost risk, a building and pest inspection may be the next cost item that a purchaser considers.

Building and pest inspections vary between inspectors. Some outsource a separate pest inspector, while many offer both in tandem. Costs range from around $500-750, and large dwellings can carry an additional surcharge.

Before embarking on this cost, a buyer needs to ask themselves two important questions:

- Are there any obvious signs of trouble that they can physically spot at the property themselves? For example, can they detect unlevel floors? Can they see any water damaged timbers? Is there a large amount of asbestos visible? These are often obvious.

- Have they conducted a sale price feasibility test for themselves?

This latter point is often the most cost-saving step a buyer can take.

Determining whether the budget will even have a chance is vital before enlisting the help of paid professionals.