Riding the storm

Plenty of investors make an early decision to sell a property. Life doesn’t always go to plan, and things can change. Today’s blog is about the decisions to sell that are later regretted.

Property is a long game. Very few investors build wealth over a short period, and often a short term tenure can trigger financial losses, particularly when stamp duty and selling fees are taken into account. Even for those investors who do manage to make a capital gain, tax treatment of that gain will erode the profit.

Over the years I’ve met many investors who have either contemplated selling or have sold. Most who have sold later had a sense of regret down the track, realising the wealth generation they’d forfeited when they decided to sell. For some, a decision to sell is based on necessity, but for more than a few it’s often based on fear or frustration.

Sadly, some of the reasons that compel investors to sell can be mitigated.

The first relates to a bad tenant experience. Feeling trapped with a horrible tenant is not that uncommon and sadly the tribunal delays and paperwork required to remove a bad tenant can leave a lot of rental providers feeling frustrated.

If the tenant has stopped paying their rent, the problem is further compounded and can trigger cashflow issues. Having a buffer account for the unforeseen issues is one step to smoothing this risk, but first and foremost, a great property manager can make all the difference. If in doubt about how to identify a great property manager, ask fellow investors in the area for some advice, or reach out for a recommendation from a buyer’s advocate who is active in the area.

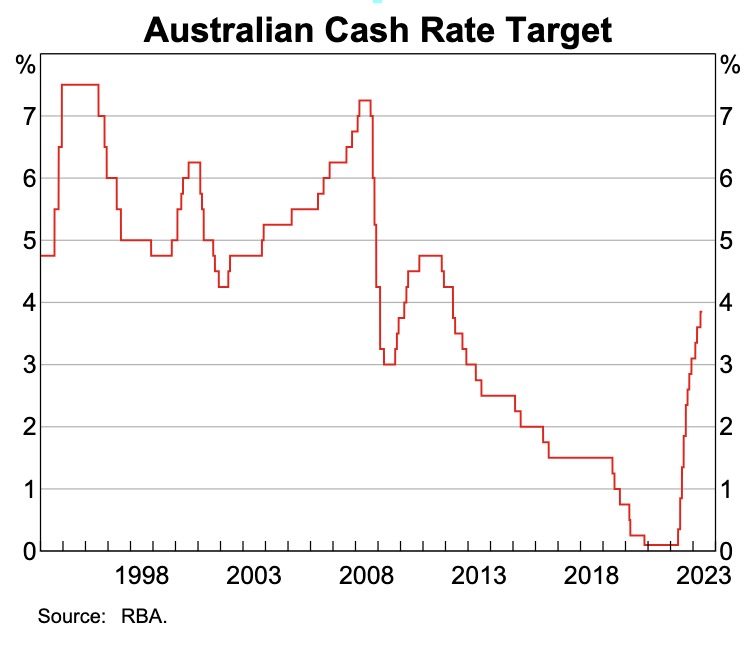

Another reason is rising costs of ownership. This is a topical point because our current interest rate movement has been heady for many property owners. Our reserve bank’s efforts to bring down inflation have not yet taken full effect and sentiment around further increases is best described as fearful.

Until our inflation figures are back down towards our target band, we can anticipate that the RBA will continue with the hikes.

What is interesting, however relates to the items that are driving inflationary pressures. It’s not simply a case of Aussies spending more on good times. We have faced price hikes for reasons beyond our control over the past year and these have indeed contributed to our high inflation rate. Fuel, transport and food and drink are non-negotiables when it comes to spending, and these items have featured significantly. Supply chain issues associated with the Ukraine war and COVID lockdowns have caused much of these woes. It is interesting (and hopeful) to note that the cost of container transport is almost back to pre-pandemic levels.

Our inflation will eventually come back down, and the pain associated with higher interest rates won’t bite for ever.

Our banks calculate borrowing capacity based on a 3% buffer rate, which means lending rates factor an additional 3% interest on top of the lender’s interest rate of the day. This wouldn’t be pleasing for those who borrowed when rates were sub-3%. Many have considered fixed rates, and as always, the decision to fix or take on variable is a personal decision that should only be discussed with a qualified advisor.

Another reason that people sell an investment earlier than planned relates to other opportunities that arise. Whether it be the decision to upgrade the family home, (or for rentvestors, to buy a home), or a chance to take time off work for travel or study, exciting things can tempt people to cash in their gains.

Thinking long term about your ultimate goals and your reasons for investing in the first place is important. Many investors I’ve met could have retained their property and found a way to have the exciting opportunity also. Clever mortgage strategy, use of offset accounts, a deeper understanding of equity and cashflow, and a chat with a qualified professional can make all the difference.

Running the cashflows before making a subsequent financial commitment is imperative.

Vacancy periods can frighten investors. These days, we don’t see many vacant properties sitting on the market, but in past years I’ve seen plenty. Even thinking back to our COVID lockdown period in Melbourne reminds us of how grim it would have been for landlords holding Melbourne apartments.

Properties are vacant for a reason. Sometimes it’s the condition, other times it could be location. But more often than not, it’s price. A poor-performer is one thing, but getting professional advice on a problematic property before triggering a sale is important. All too often I’ve witnessed rookie mistakes being made with properties up for lease and the issue could have been mitigated with a pro-active property manager.

Another reason why people sell sooner than initially intended relates to impatience. Looking for fast (or linear) capital growth is a common trap. Property performance looks a lot more attractive on a chart when the chart spans decades. Looking up close is a dangerous habit and sometimes looking at static is enough to tempt an investor to sell and reinvest the money elsewhere.

Property is a long game.

Last but not least, some people sell investment properties earlier in an effort to time the market.

However, this too is a dangerous game because the best of us don’t know exactly when a market bottoms or peaks. I’ve seen plenty of sales that were based on a belief that the market was about to fall. Take for example the panic when COVID struck. Those who sat it out, waiting for the significant price falls were disappointed after realising that 2021 delivered some of the heftiest price increases in history.

Selling an investment property earlier than planned is sometimes unavoidable, but talking to the right advisors before making a decision to sell may deliver some other options to consider.