Is Melbourne’s property market experiencing a surge in capital growth?

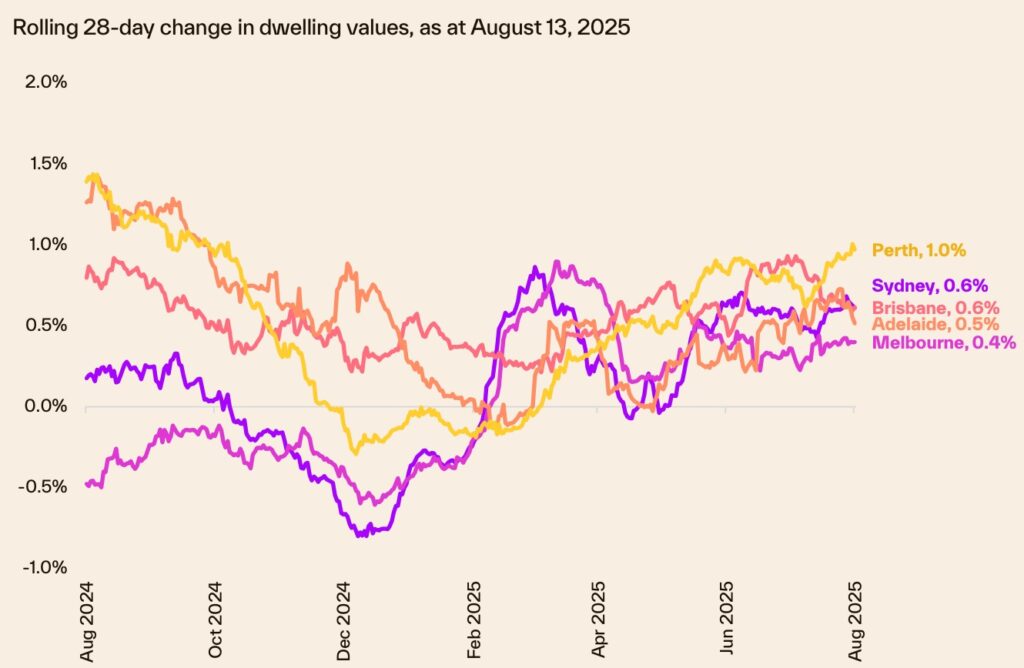

Melbourne’s reported capital growth data has consistently shown our city experiencing modest gains since the start of 2025. The monthly median dwelling value growth has hovered between 0.2% and 0.7%, with strength in the middle quartile of the market, including both houses and units.

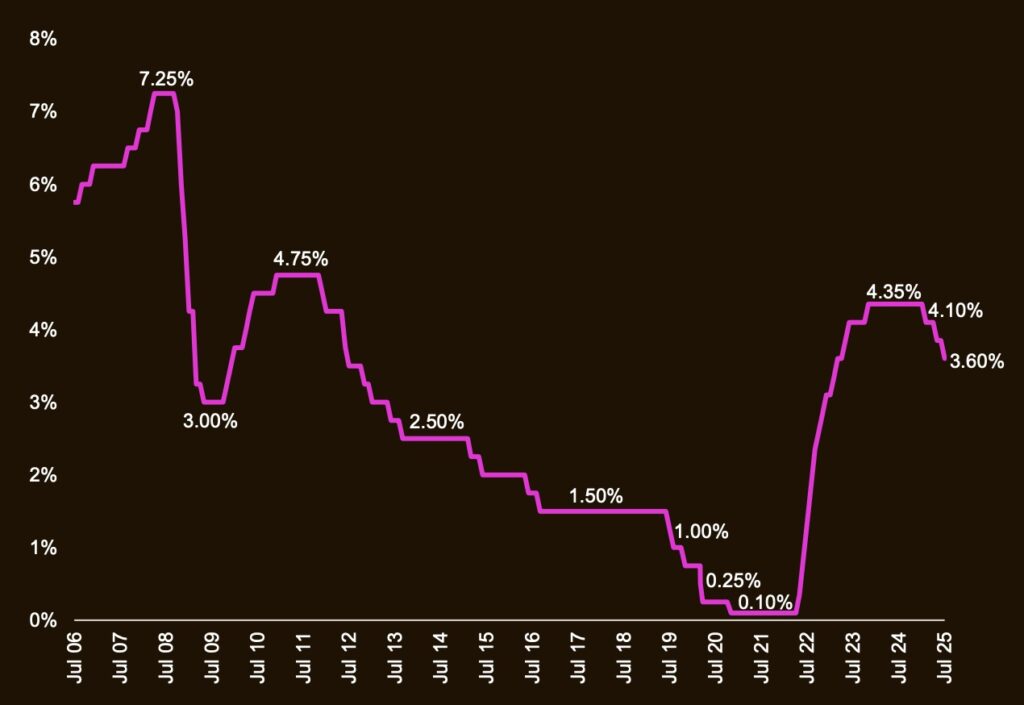

In the first half of the year, auctions felt more competitive, clearance rates have strengthened, and buyer numbers have increased. The February and May interest rate cuts stimulated the market somewhat, and buying conditions became a bit tougher.

The interest rate cut in August, however altered sentiment completely. This, in tandem with the Federal Government’s announcement to bring forward the uncapped First Homebuyer Deposit Guarantee Scheme has stimulated buyer activity and buyer budgets.

On the ground, the mood has changed.

Over the past three weeks, agents have reported a significantly increased level of buyer participation and resultant prices. At every single auction we have attended, prices have soared past our anticipated and calculated likely selling price. Records have been set in some suburbs, (Ardeer as a shining example.) Yesterday saw Ardeer’s first $1M sale of a house on a standard-sized block.

Melbourne’s lower and mid-priced housing segments are now experiencing a surge, although the data is yet to tell us this. We expect that the September market data will show a significant boost in capital growth performance when it breaks early next month.

Interest rates don’t cause a surge, but buyer sentiment in combination with heightened borrowing capacity certainly does.

A 0.25% interest rate cut increases borrowing capacity by anything from $15,000 to $50,000, depending on individual the debt level and the borrower’s circumstances. This represents a significant increase in buying power, and explains why many suburbs and dwelling types have demonstrated a fast uplift in a short timeframe.

The cash rate decision in August amplified the already-existing sense of FOMO, (fear of missing out) with many buyers fearing a surge in prices. Many of those who have become active in the market currently are doing so to beat the herds in Spring.

The lower listing volumes are exacerbating the issue, as buyer numbers outstrip vendor numbers.

Cries of underquoting are also getting louder; a common indicator of a surging market. Anecdotally, agents are frequently getting a surprise alongside their vendors when sale results exceed their expectations by a significant margin.

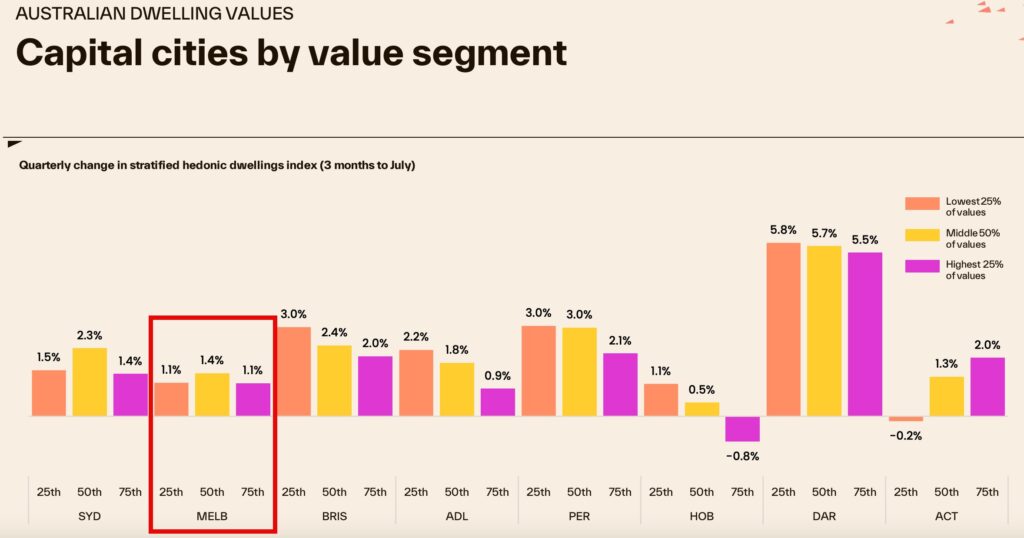

Focusing on the market segmentation is important. The data echoes what we are experiencing on the ground. The lower and medium-priced properties are in demand and there are two main cohorts who are competing with each other; first homebuyers and interstate investors.

Since the beginning of the year, our interstate investor enquiry has dramatically increased. Currently, more than half of our clients are investors. We have not worked with this percentage of investors since 2021.

In Melbourne’s entry-level, outer-ring house markets, investors have contributed markedly to the gains, and in my areas they have elbowed first homebuyers out of the way.

The first homebuyer deluge is currently underway in the sub-$950,000 market. Many are pouncing in now in the hope to beat the hordes and purchase before 1 October. We can expect that this segment of the market will strengthen quickly, and it will be the units in the inner and middle rings that also surge. Until recently, houses have outperformed units, but this changed trend has certainly been a hallmark of 2025, along with a rebounding market.

Strengthening markets aren’t all that pleasurable to buy in. And surging markets are really tough. While our current buyers are feeling the heat, I also consider the positives. Capital gains are positively impacting our past clients; those who are already in the market.

After almost three years of disappointing market conditions, these owners are now getting a reprieve.

It will be interesting to see how our Spring market fares. Until more sales listings result, the conditions will remain tough for buyers. A further rate cut will have a strong impact and we anticipate 2026 to be a year of stronger gains for Melbourne.