What does the price ratio between Melbourne’s fringe suburbs and middle ring suburbs tell us about the value proposition that is emerging?

For the last two years, Melbourne’s outer-ring, fringe suburbs have been delivering outperformance capital growth in the house market category.

While we have incentivised first home buyers with the broader rollout of the Federal Government’s 5% deposit guarantee, and stamp duty concessions remain in place, there is another reason why these areas have delivered growth.

Investors are back, and predominantly from interstate. Sydney continues to lead the chase when it comes to our interstate investor count, but 2024, 2025 and 2026 have seen strong numbers from QLD, SA and WA (in that order). Even NT investors have made an appearance, no doubt all of this activity due to huge equity gains on their homes and local investments.

The markets that have been targeted strongly by investors have been outer fringe suburbs. Some of our highest performers have included: Frankston North, Coolaroo, Dallas, Melton, Werribee, Wyndham Vale, Cranbourne West, Tarneit, Truganina and so on.

However, not many of these markets are supported by rail infrastructure, and not all can be described as aspirational.

They are best described as affordable.

Many Melburnian local buyers agents have noted the disproportionate number of interstate buyer’s agents in these locales too. Most don’t fly down. Their offers are submitted hard and fast, usually following the selling agent sending them a video.

While some may conduct their own research and arrive at a suburb, many purchase data these days. Depending on the data house that predicted suburbs are chosen, it’s not unusual for large numbers of volume buyer’s agents to target these areas en masse.

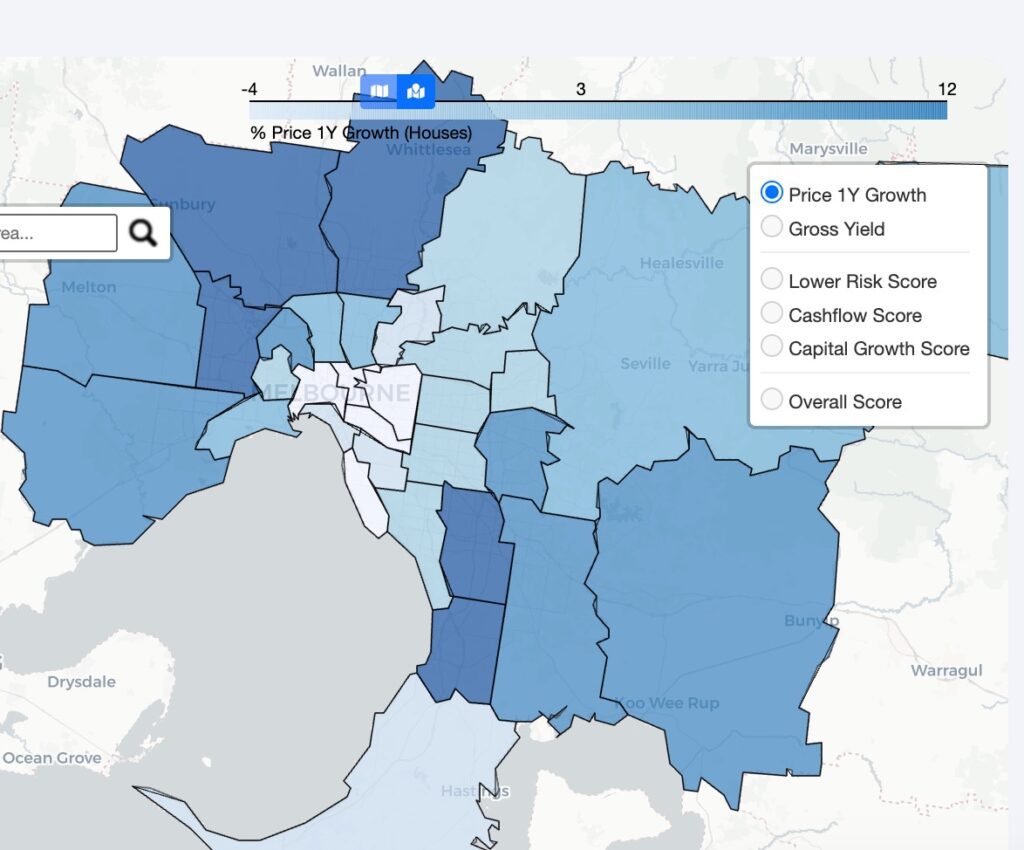

This heat map from a popular provider illustrates the theory that this particular data house supports strong performance for outer-ring, Melbourne suburbs, along with some south-eastern segments of our city.

Some of the accompanying commentary includes, “The most popular areas for property investors are the inner city units and houses around the outer circle suburbs. “The Melbourne property market is on the rise with many experts tipping it to be one of the strongest performing markets in the country this decade. The city’s population growth, stable economy and limited supply of properties are all driving forces behind the emerging market conditions.”

Is it any wonder that so many volume-based, interstate buyer’s agents are targeting our city?

However, this recent, strong growth has highlighted an interesting observation.

Some of the inner-ring and middle-ring suburbs are now representing a comparatively attractive value proposition.

Let’s take, for example, two houses in the hot list.

The house on the left is a recent sale in Frankston North; some 38km south-east of the CBD. Offering plenty of now-privatised commission houses, this suburb has delivered strong rental yields for investors, although the recent price hike for the area has reduced gross rental yields somewhat for new investors. Frankston North is conveniently close to the Eastlink tollway, but not near to rail transport.

This house on the left sold for $762,000 this month, and sits on a 543sqm block of land.

The house on the right is a newer property in Cranbourne West, some 41km south east also.

This property also sold this month for $750,000 and sits on a smaller block of 331sqm.

The land to asset ratio is much lower given the dwelling age and the land size. This is arguably not an ideal investment for these reasons, among others. Cranbourne West also is devoid of rail amenity.

If I contrast the sale of a similar sized dwelling on a similar allotment of land in a middle ring suburb, options include this recently purchased property in Melbourne’s middle-ring north; Reservoir.

This rear unit in a block of just two sold for $875,000 in February and the allotment is 303sqm, along with an undivided share of 147sqm of driveway area.

Reservoir is just 12km north, offers a vibrant shopping village, great rail amenity, Edwardes Lake and parklands, and a great gentrifying suburb outlook.

And showcasing a house on similar land to the Frankston North option above, this character gem in Sunshine North sits on 604sqm in an established street, and sold this month for $785,000.

Sunshine North is located 13km west of Melbourne’s CBD, and while it doesn’t offer rail amenity, nearby Sunshine is reasonably close by. The area is gentrifying, and it represents great value when amenity and proximity to CBD counts.

The disparity between middle-ring and outer-ring sales values has tightened significantly.

Even taking this red clinker brick character option in Oakleigh as an example, the price-differential between this aspirational option, and the affordable option is tighter than it has been in recent history.

This house sold in November last year for $1,450,000. Just 14km from CBD and surrounded by other well-regarded, middle ring south-east suburbs, Oakleigh’s amenity is impressive by any measure.

I can’t recall a time when a quality character property in a nice street in Oakleigh sold for less than double the price of a house in Frankston North.

The price ratio between similar sized land and dwellings in the outer-ring vs middle-rings is tighter than the historical mean.

Could the outer-ring areas be overheating?

And is investor-driven demand as sustainable as owner-occupier driven demand? Of course it isn’t.

The question begs: is it time to turn our attention to the middle-ring?