The Next Phase for Melbourne Rents: Forecasting 20% Growth in Established Suburbs

When policy settings shift, behaviour follows. In property markets, that behavioural change can ripple through entire segments and reshape outcomes in ways that aren’t always initially obvious to those who reshape policy.

The proposed removal of negative gearing and changes to capital gains tax for established property are significant policy levers. While much of the public conversation centres on affordability and equity, there is a deeper layer to consider, particularly across our inner ring and middle ring suburbs where housing supply is already constrained.

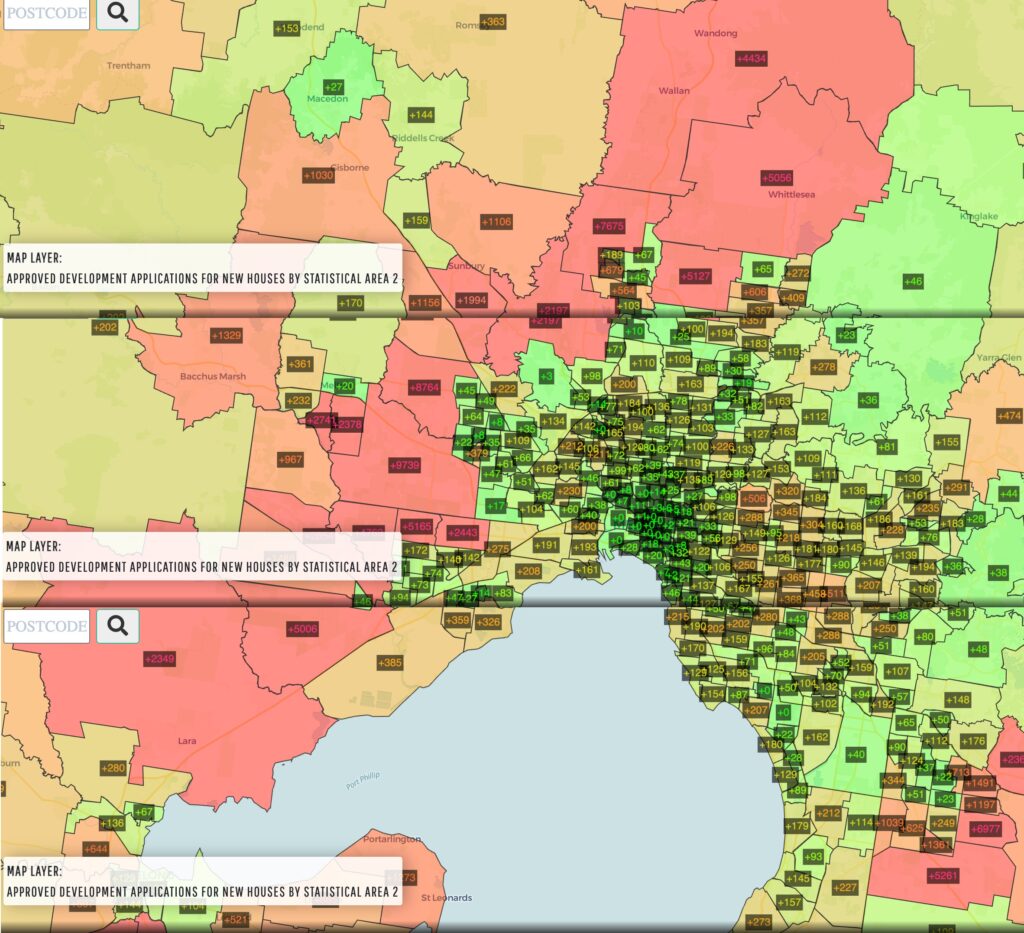

The following Melbourne Statistical Area 2 heatmap, (source: Heatmaps) shows the number of approved houses from 2020-2025. The green shows lowest volumes per region, and the red indicates the largest volumes.

The approval rate of units is a different story, but the question must be asked: what happens if established house landlords exit the market?

Timing is critical here. With a proposed start date for the indexation method of capital gains tax calculations of 1 July 2027, investors holding established property are already assessing their position. For some, the financial disadvantage of holding post-1 July 2027 will precipitate a sale. That brings forward a potential wave of selling activity as the impacted investors look to exit before the changes take effect.

Established homes in inner and middle ring locations have long formed the backbone of the rental market. These are the period houses, mid-century builds, and family homes in well located suburbs with strong amenity and access to employment. They are consistently in demand from family tenants.

If a portion of investors decide to sell, the large majority of those properties are highly unlikely to remain in the rental pool.

Changes to negative gearing will automatically eliminate most investors from pursuing such a property as an investment. The holding costs will simply be too high.

In many of these suburbs, owner occupiers are the dominant buyer group. First home buyers, upgraders and downsizers often compete strongly for these homes and are prepared to pay a premium for lifestyle and long term security.

When an owner occupier purchases an investment property, that dwelling is effectively removed from the rental market.

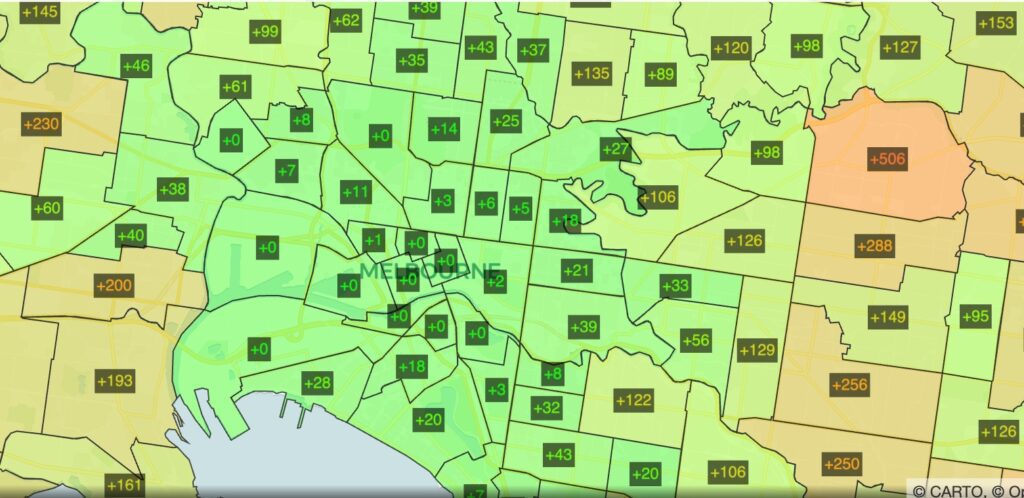

At the same time, we need to consider the supply pipeline. Building approvals for new houses in established suburbs remain relatively low. Planning overlays, zoning restrictions, heritage controls and community resistance all play a role in limiting new development. Even when projects are approved, they can take years to move from concept to completion. The following heatmap shows the limited number of new house approvals in these inner and middle-ring suburbs.

Unlike greenfield markets, established suburbs do not have the capacity to rapidly increase supply. New housing is difficult to deliver at scale and new units are often concentrated in specific pockets rather than spread across entire suburbs.

Building approvals for new houses are limited, which constrains the ability to replace lost rental stock.

If legislated, these proposed changes will create a rental house supply issue in specific markets across many of our cities.

If investor-owned properties are sold and absorbed by owner occupiers, and there are limited new houses, (or large townhouses) being approved and built, the rental pool will shrink. This is particularly relevant in inner and middle ring locations where demand for family homes from tenants is consistently strong.

The implications for renters are important. A reduction in appropriately sized rental properties places upward pressure on rents and reduces choice for those who require family-sized dwellings. Tenants who would typically secure houses in well-located suburbs may find themselves pushed further out, compromising on proximity, transport access or lifestyle amenity.

Over time, this will subtly reshape the demographic profile of suburbs as family accessibility becomes more constrained.

My prediction is that we could see a 20% increase over the next two years in rents for houses in the inner and middle-ring pockets.

For buyers, there may be a short term shift in conditions. An increase in investor listings could provide a window of opportunity, particularly for owner occupiers who have been competing in tightly held, investor-driven markets.

However, this window may not last. Once those properties are absorbed, the underlying scarcity of established houses in desirable suburbs is likely to reassert itself. Capital gains tax exempt properties include the family home, and I firmly believe we can anticipate many homebuyers opting to store more of their wealth in the family home.

Inner and middle-ring suburbs with strong owner occupier appeal are likely to see the most pronounced shift in this behaviour. These are areas characterised by walkability, proximity to employment hubs, established streetscapes and lifestyle amenity. Middle ring suburbs with quality schools, transport links and family appeal are also exposed to this dynamic.

For investors who choose to remain, and for those who enter the market after the policy changes, the landscape could look quite different. With fewer rental houses available in the inner and middle-rings and sustained tenant demand, rental yields will strengthen.

This could partially offset the reduced tax advantages, but it requires investors who can sustain higher negative cashflows, and thos with a level of confidence that not all investors will share.

It is also important to recognise that not all locations will be affected equally.

Outer suburban markets will respond differently. They typically have greater capacity for new housing delivery and can accommodate population growth more readily. The negative gearing offering for investors who purchase brand new property will likely see the outer suburban rental numbers vastly increase. However, outer suburban houses do not always provide a direct substitute for tenants seeking proximity to the city or established infrastructure.

Changes designed to improve housing affordability can have unintended consequences if supply constraints are not addressed in parallel. Reducing incentives for investors to hold established property, without significantly increasing new housing delivery in established areas, risks tightening the segments of the market that many tenants in established areas rely on. From schools, to family support, communities and clubs, many tenants will face being displaced from the areas they currently live in.

The lead up to 1 July 2027 will be an important period to watch. Listing volumes, the mix of investor-led sales, buyer segments and rental vacancy rates will all provide insight into how these dynamics are unfolding.

For participants in the market, the key is to look beyond the headlines and focus on the local trends. Understanding how behaviour is likely to shift, and how supply constraints will interact with those shifts, will be critical in making informed decisions.

In real estate markets, it is rarely the announcement that defines the outcome. It is the collective behaviour that follows.