Over the past twelve months, many have asked m when the best time to buy would be. My answer was simple. “In 2024”, is what I told them.

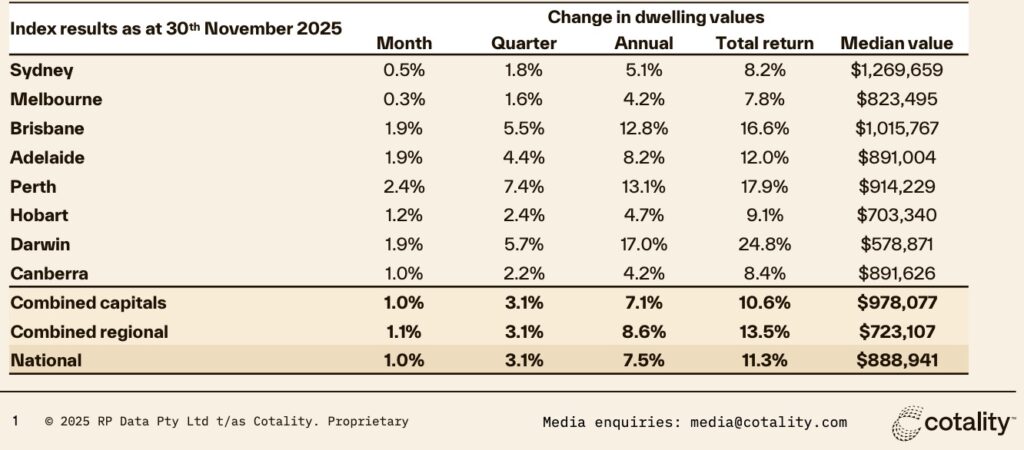

This years’ recovery for the Victorian market has been modest. Melbourne hasn’t outperformed the capital city markets by any means, but unlike the previous three years, every single month has exhibited positive growth.

However, like any generalised growth figure, the median dwelling price data doesn’t tell much of the story.

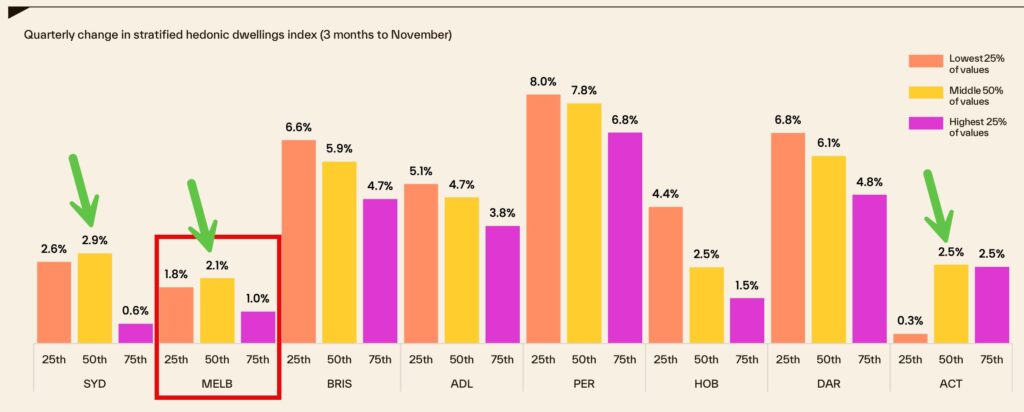

Segmenting the data tells a little bit more, and overlaying this with insights from the coal face gives a much better overview.

This chart below helps explain my 2025 summary. First home buyers were quite active, and this activity was further stimulated by the extension of the Federal Government’s 5% deposit guarantee. While many were already taking advantage of this capped offering during the first nine months of the year, the floodgates opened from 1 October when the initiative was open to all eligible buyers. Plenty pursued apartments and units, but in true Melbourne form, a large number of first homebuyers also targeted houses on freehold.

Interestingly, so did the investors. Victoria saw a very large number of interstate investors who decided that the value down south outweighed their own state’s offerings. With surging values in WA, SA and QLD, it’s little wonder that the majority of our investors came from these states. Sydneysiders continue to see value in Melbourne also, with some speculating a mean reversion to spark their investment’s growth.

As a result, our markets saw the strongest growth in the mid-price points, (for both the capital city and regional markets). Melbourne’s outer-ring housing market has shifted strongly; from Frankston North to Werribee to Epping. This array of growth suburbs is wide, and the properties in question have much in common. They are all typically brick and tile, 1970-1990 era, and on allotments of 500-700sqm.

These markets have exhibited over 10% growth in one year; no mean feat considering Melbourne’s overall median growth has been clocked at just over 4%.

The Victorian markets represent opportunity in 2026, and plenty of people are asking me what my best tips are for the new year.

This coming year, I’m circling houses and units with great bones, and terrible interiors as the future prizes.

For over seven years, our city has been busy with civil infrastructure projects. Billions of dollars have been spent on tunnels, by-passes and a new train system. Many private tradespeople have taken on roles within these projects, and in tandem with the COVID-driven materials shortage, our labour shortage has impacted our market enormously.

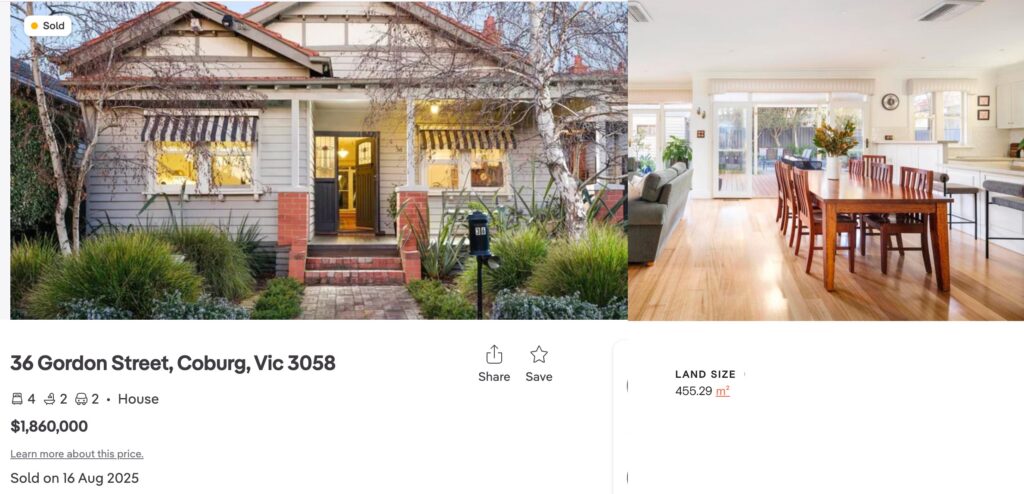

Renovations have been broadly avoided due to excessive costs. Buyers have shifted their preferences from renovation projects to renovated purchases. Those who have bought ugly duckling houses over the past few years will be rewarded. The cost differential ratio has been at it’s highest. In other words, the discounting on renovation projects has been at it’s highest, and the premium for renovated products has also peaked. These two dwellings which sold at a similar time in 2025 are a great example of this.

The two houses sold within eight weeks of each other. The move-in ready house had strong competition and sold for $1.86M. Offering 90% of the land size of the one below, the price differential is even more compelling.

The renovation project below had less competition, and couldn’t easily be described as move-in ready. In fact, it needed some initial, ‘interim’ works for our clients and their young family to make it comfortable while they arrange plans and permits for their renovation. However, the relative discount will make their sacrifice worth while.

As tradespeople re-enter the private market and materials cost-surcharges slow, we can anticipate renovation costs will ease also.

The ugly duckling opportunities are abundant, and selecting a well-located dwelling with ‘great bones’ seems the next obvious opportunity for buyers.

I predict that the cost differential between ‘renovated’ and ‘requires-renovating’ will shrink over the course of the year. I also predict those who are happy to take on a liveable ugly ducking will fare well into the not too distant future.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU