Buying at the bottom of the market cycle

This is such a dilemma for so many. In principle, it sounds so good.

If only we could have the courage to do so, yet most don’t.

All of the market leading indicators in the world won’t take away from the fact that when a market has fallen, prospective buyers are generally more fearful of further declines than they are excited about a potential bargain buy.

The last three years have reminded us all of this. What is really compelling is that even with two consecutive market falls (literally within less than twelve months), human nature for most buyers was to run for cover and wait it out.

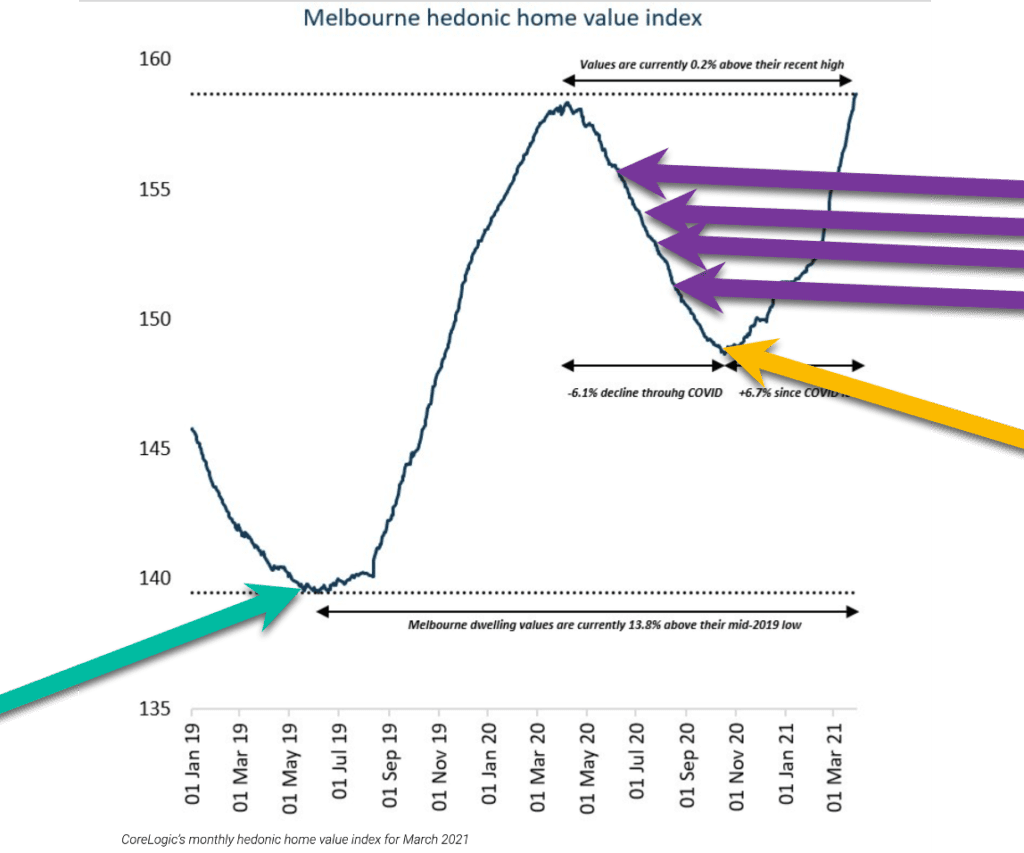

Some of the people who had said to me “I wish I’d bought in May 2019″ still ducked for cover and put their plans on hold in March 2020 when COVID struck.

It’s of little surprise that market jitters are putting buyers off today, only two and a bit years since our last opportunistic buying season.

Last year our markets nationally outperformed, delivering the third highest capital growth rate over the past fifty years. People were excitedly jumping on the bandwagon, vendors were revelling in the favourable market conditions, and newsfeeds constantly quoted FOMO as a market force.

Money was so cheap, household savings were up as a result of lockdowns and limited travel expenses, and households were making considerable decisions about their abodes.

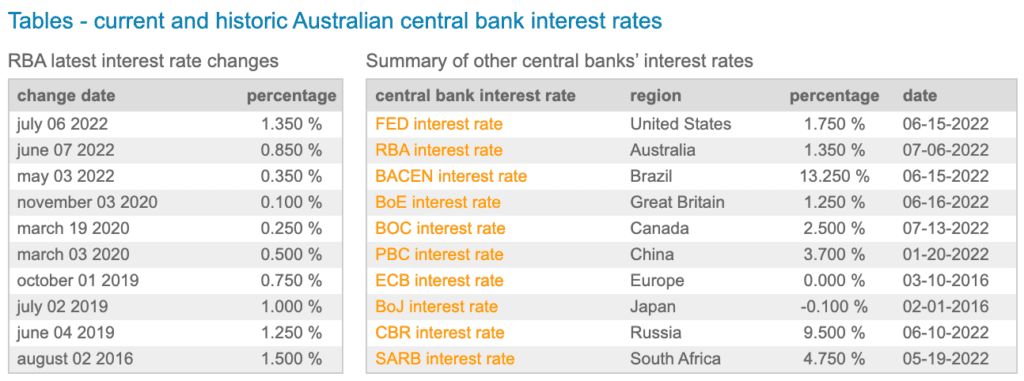

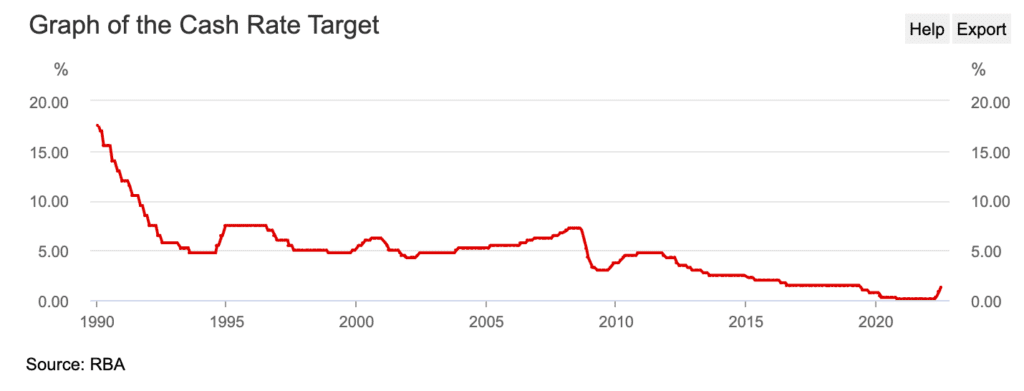

Suddenly we had news of Russia invading Ukraine, inflation woes in the US and chatter about increasing interest rates. As our Federal election loomed, our RBA did the unexpected and increased the cash rate just before we hit the polls. The first rate increase rattled a few, but most buyers carried on with their searching. However, the second rate increase did increase the jitters, and by this time, all capital city markets had peaked and their rate of growth was slowing across the board, with Sydney and Melbourne reporting modest declines in median dwelling values. The third, and significant increase however startled prospective buyers even more though. A full half percent increase felt signifiant after eleven years of cash rate reductions.

Keeping it in perspective though, our cash rate remains very low by global standards and in comparison to the heady 80’s and 90’s, we are still very much in a ‘cheap money’ environment.

Sadly, many news headlines would have us believe otherwise. But as we know, bad news sells.

Do we blame the media? Or should we blame our RBA Governor for doing an about-face on his predictions for rate increases? Or….. do we consider some of the drivers that will reinstate capital growth again one day?

What I did observe back in 2019 and 2020 were the hallmarks of a tipping point in a market. Being at the coal face certainly offers a direct insight into changing sentiment, and while I’d love to say that we can pick a turning market, the reality is that we’re usually working in a two/three week delay. Sometimes the turnaround can be dramatic and very rapid, in which case our ability to pick the shifting sands is more challenging. However, looking back at the drivers is important. Supply and demand is a fundamental consideration, but the drivers that initiate a power-shift from seller to buyer, or vice-versa are the real considerations.

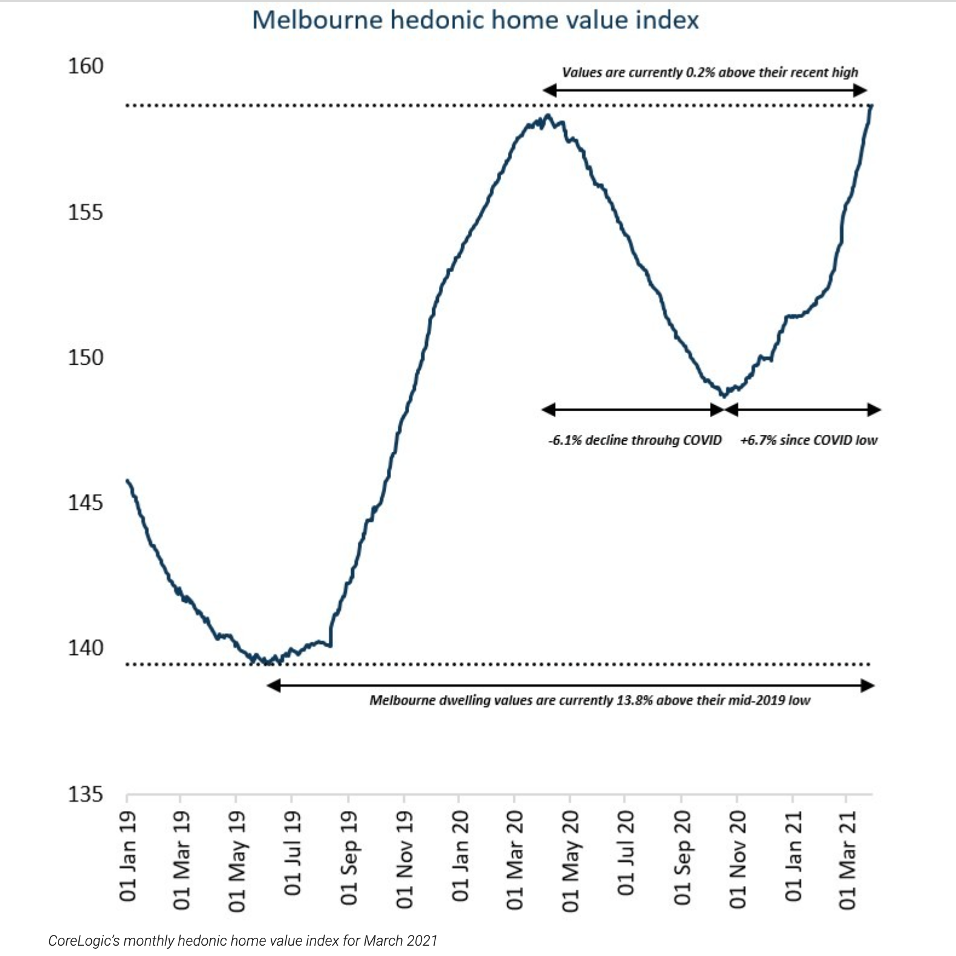

In 2019, (and pretty much in tandem), credit eased at the same time as proposed tax reforms were dropped. Money was very cheap, (although the cash rate was 1.5%; still at a higher cost than today’s cash rate). The market took off and our rate of growth was so heady, we found it challenging to appraise properties without applying capital growth overlays to sales that were older than a few weeks.

Fast-forward ten months and a pandemic was declared.

This time, the threat was unknown and every finance market report used the word “unprecedented”. People were scared, justifiably. The one key thing that could threaten property prices was unemployment. We were all worried about job security, income, workflow, and for those of us who are self employed, the enormity of the threat felt overwhelming. Our government stepped in and offered assistance; from small business handouts to Jobkeeper payments. Many of us were in lockdown and finding ourselves acclimatising to working from home. As this new way of working became our new norm, (and for some cities, a longer term outlook than just a temporary health order), our needs within our abodes changed too. In perfect synchronisation with emergency interest rate cuts, buyers who had stable employment, (and in particular; those who had increased workloads as a direct result of the pandemic), came back out and started buying property.

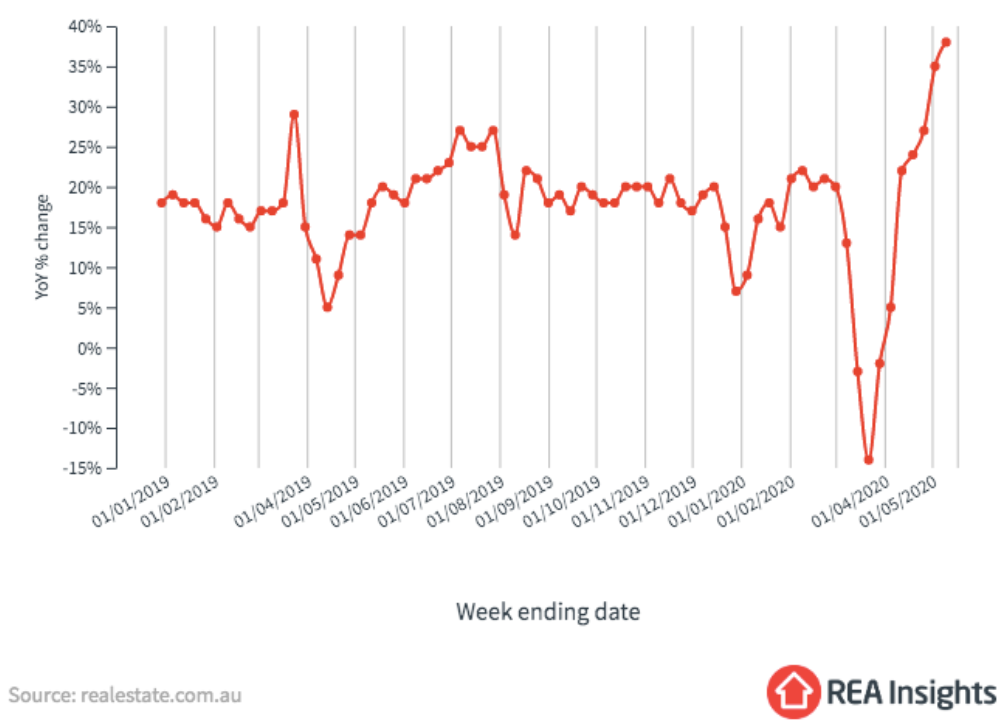

In what can only be described as a very rapid bounce-back, our markets regained quickly in mid 2020. Even with lockdowns threatening the ability to inspect and transact, buyers were a force to be reckoned with. REA buyer search activity reflected the sentiment felt during this time.

I reflected on these two difficult periods and our client experiences at the time. Most put their searches on hold, while some persisted. I’m certain it wasn’t an easy decision for those who decided to press-on, as the media hype and scary news headlines were abundant. Back in 2019 we worked with a determined investor who decided to take the opportunity to buy a single front dwelling when the price falls enabled his townhouse budget to qualify for a house budget. In the eve of the Federal election, his decision was bold.

Our investor secured the property next door to this one below, only five month’s earlier for a price 20% lower. His property condition was slightly superior and dwelling/land size identical.

During the start of the pandemic, our client book unravelled yet again, with so many placing their search on hold. One bold investor from Sydney decided that it was a good time for him to invest. We supported him with four consecutive purchases of high quality properties, inclusive of two period houses in Melbourne’s inner north and inner west, a period four bedroom house in Geelong West and arguably, the last sub-$400,000 two bedroom villa unit in Geelong West.

His risk profile was totally at odds with the herd, and looking back, his gains over a very short period were noteworthy. His employment was secure, his funding was well-coordinated and his long term goal was clear.

Another couple during this period managed to buy their three bedroom home in Seddon for $875,000; a price we would have considered impossible pre-pandemic.

When I looked over our client purchases, the one client who did manage to time the very bottom of the 2020 cycle was also an investor from Sydney. He purchased this townhouse on its own title below, and our special conditions were particularly creative. At this stage Melbourne was only just coming out of lockdown and I’d managed to apply a “subject to Cate inspecting it” condition to the offer.

What all of these buyers managed to do was to make a bold decision to buy in the face of particularly negative market sentiment.

Did they know they’d timed the market perfectly at the time? Probably not.

What we need to look at now are the drivers that are likely to aid a market recovery. Unemployment is not a threat in this current environment. Supply chain woes are likely here to stay for a while longer, placing further pressure on existing, renovated dwellings. Stock levels are tight, and vendor appetite to sell in the current market is low. When will new arrivals grow in number, how will return-to-the-office unfold, how will our tight labour market play out, and what can we anticipate from returning investor numbers?

For those out there who are trying to time the market, a feasible question to ask yourself is “could now be that time?”