Now that we’ve seen the RBA pivot to rate cuts after a period of tightening, the question on every buyer, seller, and investor’s mind is: What does this mean for the property market?

The answer depends on a lot of variables, but segmenting areas by price point is an interesting consideration. Rate cuts tend to impact the lower, middle, and upper price tiers differently after a period of tightening.

1. Entry-Level Properties: First-Home Buyers Get a Tailwind

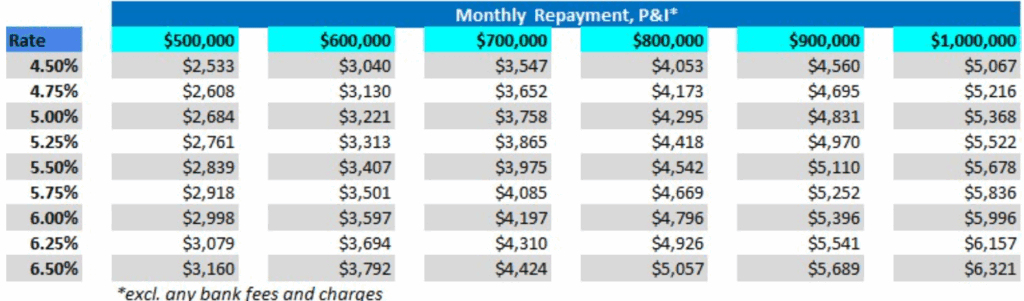

Rate cuts bring relief to all buyers, but particularly first-home buyers. This cohort is usually the most sensitive to borrowing costs, with tight budgets, lower incomes, and minimal buffers. When rates fall, their borrowing power increases—and sometimes quite dramatically. A 0.25% cut in interest rates can translate to tens of thousands more in potential loan size, as shown in this table below. (Thanks to Tim Boyle from Tri-State Finance). Tim cites, “For every 0.25% cut, I estimate borrowing capacity should increase by 4%.” For a $600,000 borrower, this translates to around $24,000.

In Melbourne, that can mean the difference between a basic apartment in the outer suburbs and a small villa unit in a middle-ring suburb—often with better long-term capital growth prospects. This shift will spark competition in the sub-$700K market, particularly in areas like Werribee, Melton, Hoppers Crossing, Sunbury and parts of the outer southeast like Frankston North and Karingal.

But the competitive landscape for first homebuyers is changing.

Since 2022, Victorian first homebuyers have had an advantage over other capital cities. Investor interest declined sharply following the interest rate hikes between 2022 and 2023. In tandem with land tax increases and tough rental reforms, Victoria experienced a decline in investor stock. First homebuyers experienced limited competition from investors and the data reflected this.

Fast-forward to 2025, investor interest is increasing in Victoria. This is due to a combination of factors, ranging from sentiment, (mean-reversion theory), increased rental yields and an obvious value proposition.

Many interstate investors returned to Melbourne in late 2024, searching for opportunities for houses in the affordable markets. Typical budgets were (and still are) in the sub-$700,000 range, adding competition to first home buyer locations.

With speculation suggesting more interest rate cuts are to follow, we can anticipate more investors and first homebuyers circling some of locations in the sub-$800,000 market. Some examples include Altona Meadows, St Albans, Thomastown, Lalor, Chirnside Park, and Carrum Downs.

2. The Middle Market: Upgraders Re-Enter the Arena

The mid-tier market, (properties between $1 million and $2 million), tends to be the domain of professional first homebuyers and upgraders. First homebuyers in this price segment have either been saving for longer, or benefited from a generous helping hand. A larger proportion of buyers in this segment, however are upgraders. They have equity in current property and are now motivated by life stage changes: a growing family, school starts, or work-from-home needs.

This upgrader segment is less driven by interest rates than first-home buyers, but still quite responsive. Rate cuts help by easing the leap from one mortgage size to a larger one, particularly for those who have seen equity gains in recent years but were holding back due to high repayments.

The suburbs where this shift becomes visible include many parts of the inner west, inner to middle ring north, (such as Coburg and Preston), and pockets of the middle ring south/east such as Bentleigh East, Glen Waverley, Mordialloc and surrounds. These areas offer family-sized homes, good schools, and access to transport—all things that attract the upgrader market.

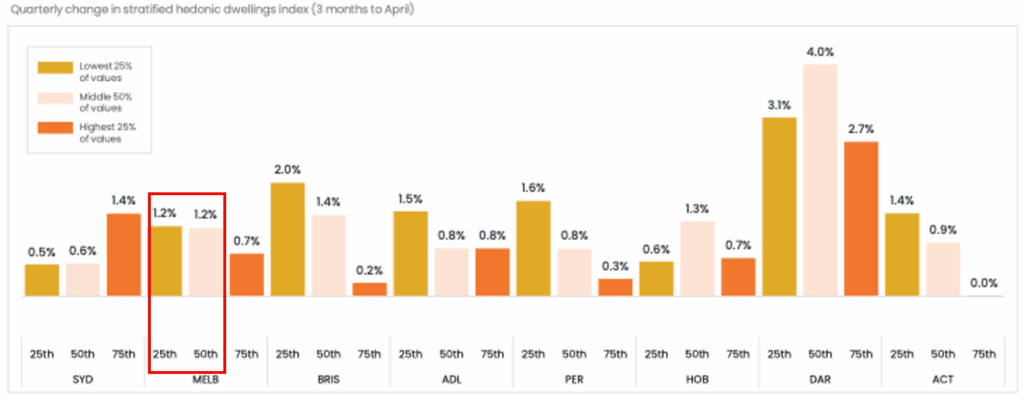

This recent chart below from CoreLogic below demonstrates the demand for bottom and middle quartile price-points in Melbourne. Typically, during downturns it is the lower priced houses that are more resilient in Melbourne, but when credit cycles loosen in tandem with a market recovery, it is the higher priced properties that exhibit the strongest growth in percentage terms.

When rates fall, mid-tier buyers become more active. That increased competition, particularly for renovated homes can push prices up quickly. Vendors take note of stronger clearance rates and often adjust their expectations accordingly. This will remain a challenge for upgraders during the winter months of 2025 where this market quartile will likely experience a demand that outstrips supply.

Interestingly, mid-tier homes can also draw in some investors—particularly rentvestors—who now see better cashflow potential as borrowing becomes cheaper and servicing levels increase. Melbourne’s heightened rental yields are also aiding investors in this market segment.

3. Prestige Market: Confidence Returns, But Timing Is Key

The top end of Melbourne’s market is a different beast altogether. Properties priced north of $3 million operate more on confidence and sentiment than strict borrowing capacity. Buyers in this tier often have diversified wealth, stronger equity positions, and access to private lending or cash reserves.

That said, interest rate cuts still play a role. They affect the broader economic narrative—consumer confidence, stock market performance, business profitability—all of which influence high-net-worth buyers. When the financial mood brightens, so too does activity in blue-chip suburbs like Toorak, Brighton, Fitzroy, Middle Park/Albert Park and South Yarra are all home to these price points.

We also tend to see expats reappear when borrowing becomes more favourable and the dollar softens (as it sometimes does in a rate-cutting environment). These buyers add to the demand pool, often in very specific niches such as the suburbs listed above

But it’s worth noting: prestige property doesn’t always react immediately. There can be a lag as confidence takes time to return and discretionary buyers weigh up their options. The result is often a slower uptick in listings and prices—followed by sudden heat in tightly-held streets and suburbs. Stock shortage can also play a key role in suburbs such as these. Homes are generally held for longer tenures, and supply and demand imbalances can give way to sales results that appear irrational.

Rate cuts create ripple effects across many cities and regions, but those ripples aren’t uniform.

For anyone considering a move in this environment, the key is preparation. Understand where your budget and criteria set applies within the market, know your borrowing capacity, and be proactive. Rate cuts can create opportunities, but panic and FOMO, (fear of missing out) can lead to expensive mistakes.

As always, good advice and clear strategy make all the difference. If you’re unsure how rate cuts affect your property plans, it’s worth chatting to a strategic mortgage broker.

REGISTER TO OUR NEWSLETTER

INFORMATION

CONTACT US

1A/58 ANDERSON STREET,

YARRAVILLE VIC 3013

0422 638 362

03 7000 6026

CATE@CATEBAKOS.COM.AU