How is lockdown *different* this time?

We all groaned when Dan Andrews announced Stage 3 restrictions last week. Parents felt that pang of anxiety at the mere thought of containing young children in the house while juggling work pressures. Small business owners, (me included) scrambled for clarification of enforceable work changes and our teenage children rolled their eyes and wondered if 2020 would ever give them a decent school holiday to enjoy.

But despite the upset and the reality of the COVID-19 impact on business and lifestyle, real estate hasn’t experienced the same, horrible shock that it did back in March.

Of course, there are plenty of similarities we can see;

- Agents are facilitating plenty more inspections due to our ‘one at a time’ rule,

- Scrambling vendors and their agents bought a large number of auction dates forward over the 36 hour period following our premier’s announcement,

- Auctions are being converted to Expressions of Interest campaigns or are facilitated via online auctions, and

- Some buyers are opting to sit it out like last time

Things aren’t exactly the same this time round.

This particular lockdown is only affecting Melbourne and one northern shire. Our regions, including Ballarat, Bendigo, Geelong are not under Stage 3 restrictions.

The property market is not responding to the restrictions like it did in March.

There are quite a few reasons for this, and while some buyers are opting to sit it out, our stock shortage, low interest rates, strengthened consumer sentiment and most of all, our confidence based on the stark difference for Australia vs US and Europe in terms of how we have so far managed to navigate through COVID-19 is palpable.

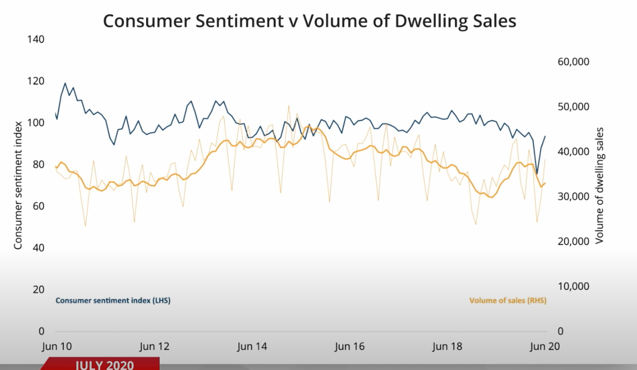

The regained consumer sentiment is evident at the extreme right (in blue)

Unsurprisingly, Australian consumer sentiment correlates with the volume of sales, (lighter shade of yellow) behind the smoothed line.

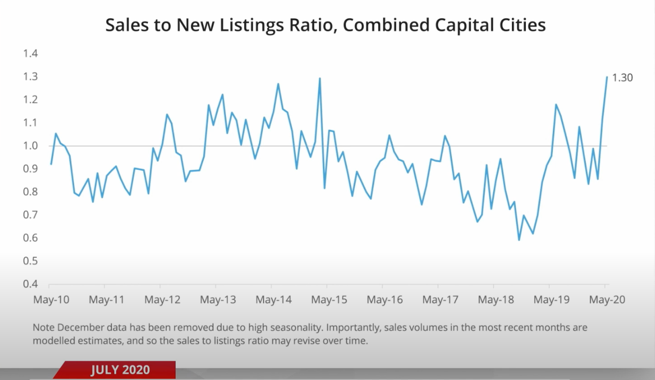

Interestingly, our Sales to New Listings Ratio for our capital cities shows an underlying demand/uptake, with 1.3 sales for every listing; a notable measure of our supply:demand equation. This is particularly useful when applied to Melbourne, as it is increasingly difficult to rely on auction clearance rates now that public auctions are not permitted.

Even with a decrease of some consumer’s confidence in Melbourne since last week’s increased COVID-19 restrictions, the current level of supply and demand is significant.

We can anticipate that for now, listings are being quickly mopped up by plenty of hungry buyers.

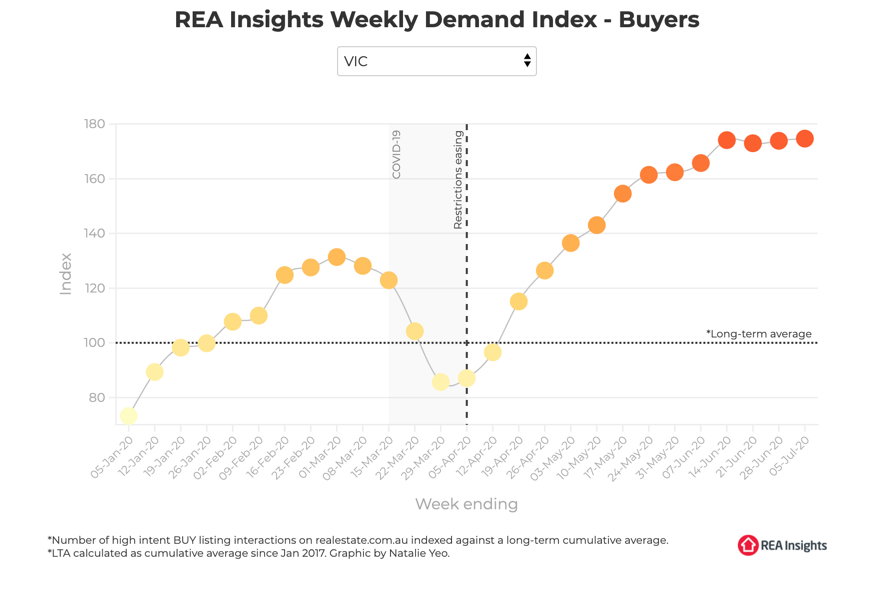

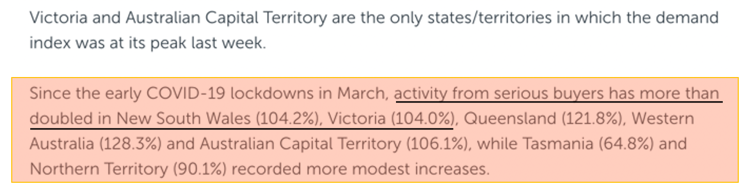

REA (realestate.com.au) has been tracking this ratio also, and with the aid of their Weekly Demand Index, we can identify in real time the consumer confidence levels within our market, both statewide and nationally.

To clarify how REA have categorised the weekly demand, the following description helps explain. The measure is not entirely specific, but the algorithm which combines visits, elapsed time, saves, multiple visits, shares and enquires certainly hints at something tangible.

What is interesting this month, however is the robust bounce-back that our market enjoyed following the initial shock of COVID-19 in March and April.

Reflecting on how things felt back then, versus now is interesting. Observations that are DIFFERENT this time include:

- Limited/zero tenants asking for rental reductions (which, initially felt like a horrible avalanche in March/April for a few weeks),

- Less stock already on market compared to March, (which was leading into the pre-Easter auction season at the time). Seasonality is definitely noticeable here in Melbourne where winters volumes are much lighter anyway,

- Many buyers are pouncing in because they recognise that SLIGHTLY softer conditions won’t last long once we get a grip on our numbers and slow our COVID-10 cases. The market bounced back and stayed firm after April as shown above, particularly in our inner and middle ring markets,

- Banks are harsher now than they were in March and April. More buyers, vendors and agents are accepting that finance clauses are almost the norm.

Back then we didn’t know how badly COVID-19 would hit Australia. The devastating news reports of the high number of deaths across Italy and Spain was scary for us all. We have a calmer view now that our hospitals are prepped and our ICU cases aren’t matching the horror of those overseas.

We were fearful about the impact on business and our economy locally and we had rumours of lockdown spanning six months. The reality is that we were locked down for some eight weeks and the real estate market held relatively firm in the capitals. The likely price falls that were documented in the media didn’t eventuate.

This time we have experience, perspective, a nominated and clear lockdown period, and talk of further support/stimulus for Victorians. Real estate agents seem more calm about navigating their campaigns.

The way that we facilitate transactions now is no longer something we’re pioneering through covid. We understand it and can adopt doing things differently.