How is Melbourne faring?

Melbourne has faced a lot of headwinds since 2020. This city has historically fared well, but the last two years have been tough.

What has caused this? How has it impacted our market? And what does the future hold for Melbourne?

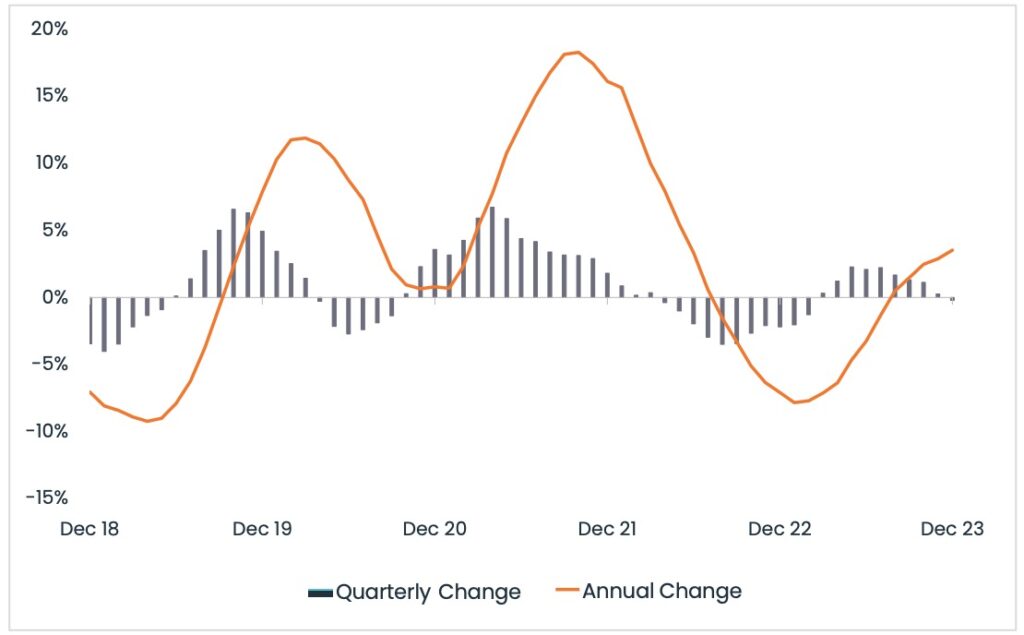

Melbourne’s growth was stellar during several points in time. Recent runs include the 2015-2017 period, post-GFC, and of course, the most recent months of 2021 and early 2022.

Melbourne’s extended lockdowns were difficult though, and sea-change, tree-change and domestic migration had a strong effect on the city. Unlike most other states, Victoria was also impacted by onerous rental reforms and land tax increases. Queensland, too was momentarily hit with land tax changes, yet the state government repealed these changes in a matter of a few months after strong lobbying and national attention shone a negative spotlight on the decision.

It’s fair to say that Melbourne (and parts of Victoria) have been hit hard with a trifecta of challenges since lockdowns eased, these being:

- increased holding costs, (interest rate increases in the face of comparatively low rental yields),

- unbalanced rental reforms that restrict investor’s control of their asset

- the new ‘temporary’ land tax, commencing on 1 July

Over recent months we have seen record numbers of investors selling. What is interesting however, is the number of new investors contemplating investing in Victoria. Anecdotally, we have had many discussions with prospective investors from interstate locations, (mostly Sydney), and some expats who are contemplating their next home upon return. They have all cited the current disparity between interstate median house prices, some spotting Melbourne as an opportunistic buy.

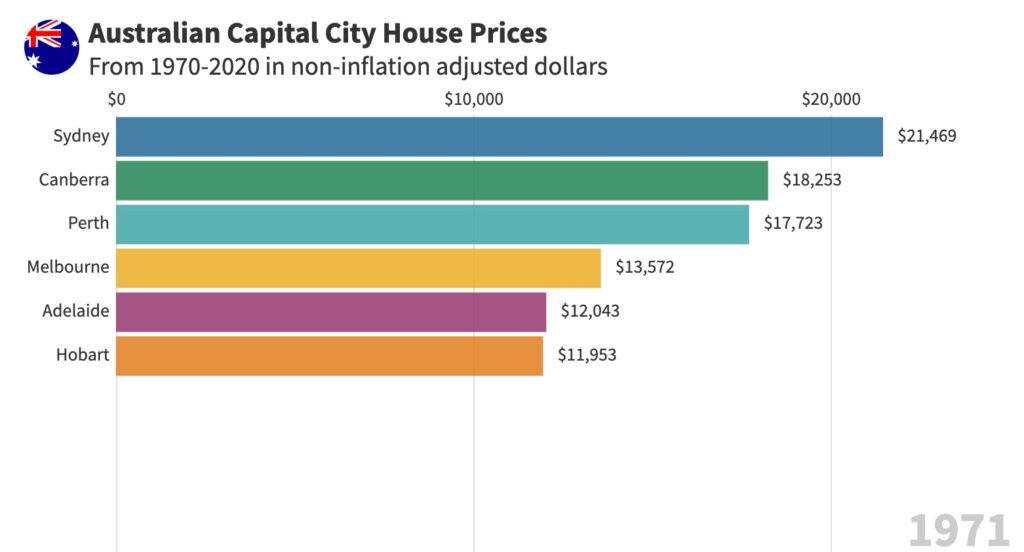

This time travel chart illustrates the elasticity between median house price ratios superbly. While it only spans 1970 to 2020, it shows that Melbourne hasn’t always historically sat in second place on the league ladder for median home values.

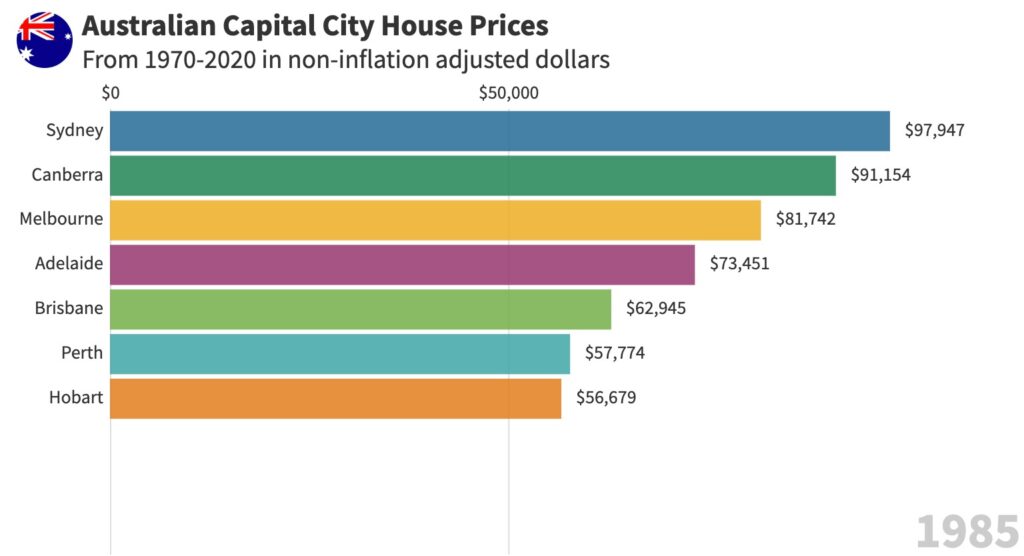

Back in 1971, the year my parents got married, Melbourne was fourth on the ladder, with a sizeable ratio of 63% when contrasted against Sydney.

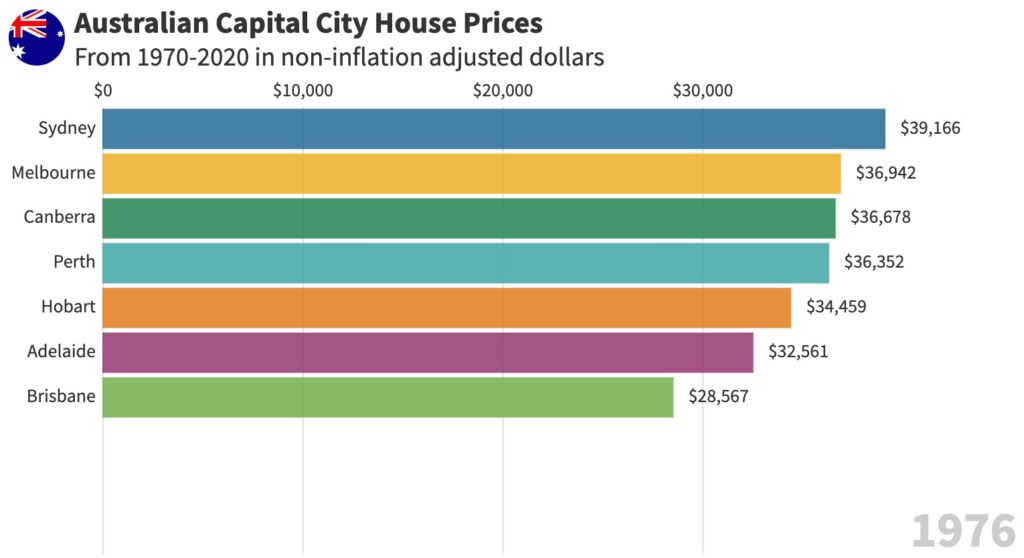

Only five years later, (when I was two), Melbourne had bounced back to second position, with a tiny margin dividing our city from Sydney. The ratio in 1976 between the two cities was just 94%.

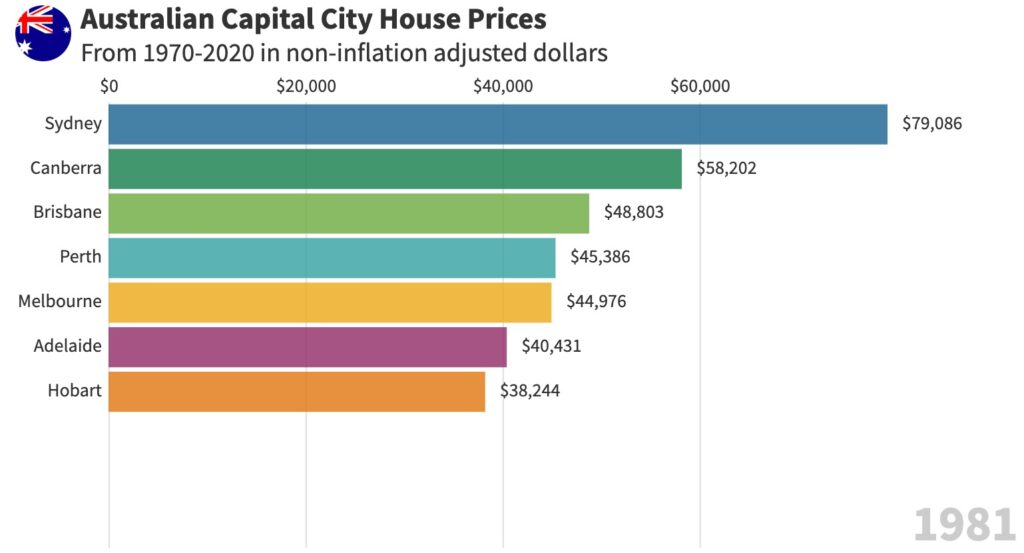

Five years later, Melbourne’s median house price had been overtaken by Canberra, Brisbane and Perth. Little did we know that Perth would pack a mighty punch some 25 years later and challenge almost every capital city. In 1981, the year before Michael Jackson released the album Thriller, the ratio between Melbourne and Sydney’s median house prices was 57%.

Only four years later, when Dire Straits released Brothers in Arms, Melbourne’s median house price growth had bounced back up to third place, while Perth had dropped back to number six. The Melbourne-Sydney ratio sat higher again at 83%.

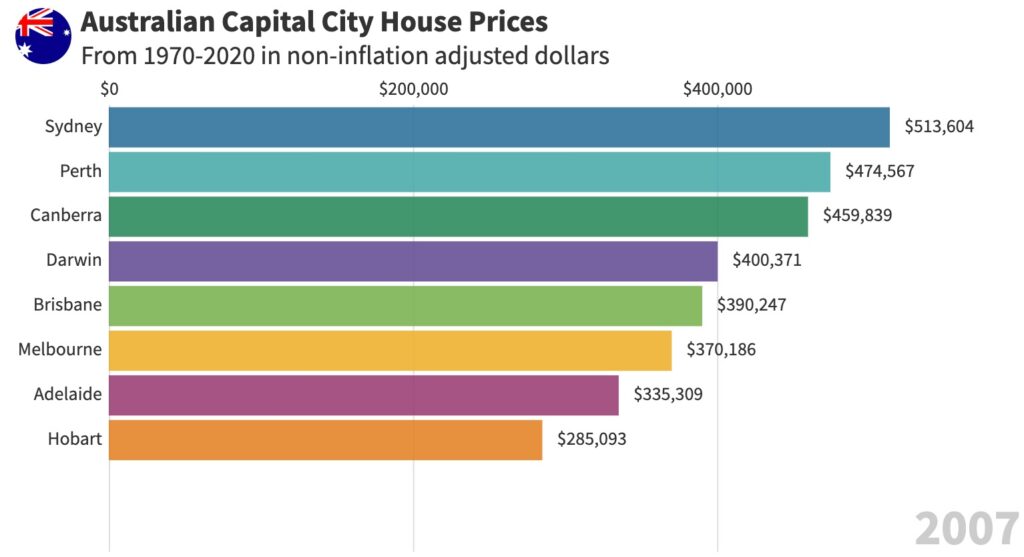

Fast forward over twenty years, just one year before the global financial crisis, Melbourne sat in fifth place on the league latter, with Perth’s impressive growth run almost challenging Sydney. The Melbourne-Sydney median house price ratio in 2007 was 72%.

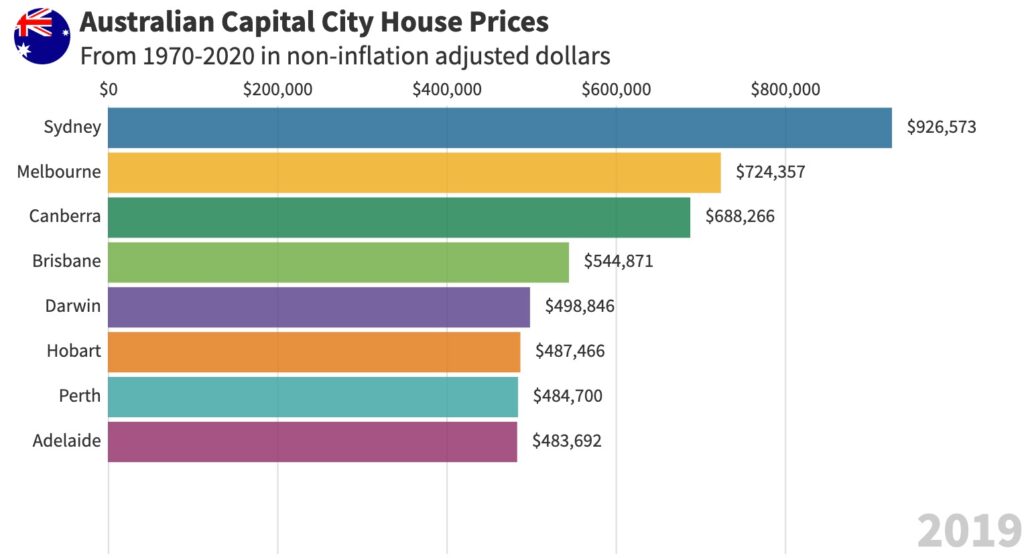

And lastly, in 2019, following a market slowdown and surprise election result, Melbourne once again took second place, trailed closely by Canberra. At this time, the Federal election surprise win could be put down to a number of policies, but the significant policy that cost the Labour Government included the abolition of negative gearing. Following May 18 that year, house prices grew and Melbourne fared well. In 2019, the Sydney-Melbourne median house price ratio sat at 78%.

The point of pointing out the league ladder and the Melbourne-Sydney median house price ratio is to demonstrate the elastic relationships between capital city price movements.

Property as an asset class is quite different to others. The cost of trading, (stamp duty and marketing/selling fees) limits an investor’s ability to make profits in the short term, and regardless of these costs, timing markets is particularly difficult to do.

Any investor who reconciles their property portfolio over a shorter period than several years is doing themselves an injustice. I’ve always maintained that any holding period shorter than five years is unsuitable, and my preference is for a holding period of greater than ten years. In fact, decades.

Property investing should always be a long term strategy, and patience is key.