One of my early, (and tough) lessons in property investment

I’ve talked extensively about my personal experience in property long before my career in Buyer’s Agency began. I’ve shared plenty of ups, and plenty of downs. Most importantly, I have enjoyed sharing my learnings, because there is a lot of merit in saving someone else the hard lesson, (and the repercussions).

I have purchased not one, but two off-the-plan properties in my lifetime.

Certainly not in recent decades, but the memories remain sharp.

The first was my very first purchase. I was still at university and I could have purchased an established house, but my worried Dad talked me out of it. Enough said. I think he’s still upset that I wrote about that in my book. We try not to discuss it.

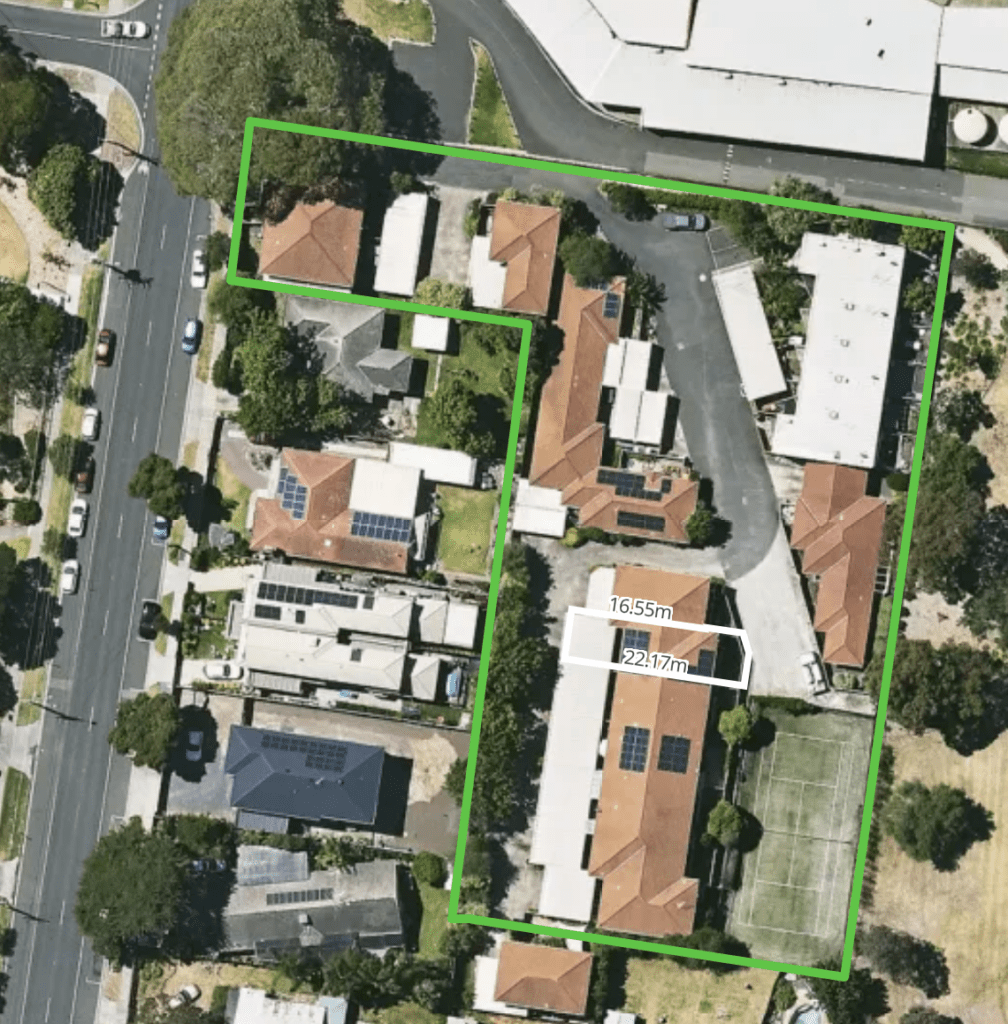

The alternative to buying the house in East Bentleigh was the townhouse in Mordialloc. This was what I pivoted to all those years ago.

Despite being an off-the-plan purchase, the location and development size worked in my favour. There were just 21 townhouses in the block, and we even had a tennis court to enjoy. The owner’s corporation fees were not excessive and the beach, train station and local shops were all within walking distance.

As far as townhouse locations go, this location was great.

Fast-forward the eighteen months that I had to wait for the build to complete, the experience continued to deliver positives. I signed a contract to purchase unit 13 for $155,000. By the time the townhouse got to lockup stage, the real estate agent called me to ask if I’d consider signing the contract back over to the builder for $185,000.

I’d put down just $1,000, and in one year I’d effectively made $30,000.

To put this into perspective, I was in my first year of employment as a graduate chemist and my salary was $32,000. I was still house-sharing with my brother and my expense were very low. Of course, I thought off the plan was fabulous. What 22 year old wouldn’t?

Then in my late twenties, I was introduced by a friendly guy at work to a development project in Melbourne’s inner north. Unlike my medium-density townhouse in Mordialloc, this project was vast, and the marketing and sales budget was significantly higher than what I’d experienced. As was the legal budget.

Unbeknown to me, I signed a contract for the purchase of a four bedroom townhouse for $545,000 with a lot of restrictive conditions. The purchase price was a much more significant price tag than I’d been used to, but I was quite dazzled by the planning and infrastructure that this project promised.

Fast-forward four years, (big projects take a lot longer), my life had changed. I was not only married and grappling with multiple mortgages. We had a child and I was on maternity leave. In tandem with my exciting life events, my career had taken a change too. I was a mortgage broker and my understanding of lending policy, capital growth, off-the-plan risk and fiscal management was far stronger than it had been when I signed the purchase contract alongside my husband.

It’s fair to say we’d had a massive change of heart about the off-the-plan townhouse.

Another Less-known Risk of Buying Off the Plan… How Developers Control On-Selling Before Settlement

Off-the-plan property can look irresistibly appealing. Glossy brochures, designer kitchens, promises of capital growth, and the allure of “getting in early” often combine to create a compelling sales pitch. For some buyers, particularly first-timers, it can feel like a clever shortcut into the market.

But after many years representing buyers, I’ve learned that off-the-plan purchases carry a unique set of risks. Many of these risk only become apparent long after the deposit is paid. One of the least understood, and most consequential, is the way developers tightly control both the publication of sales data, and the buyer’s ability to on-sell prior to settlement.

We did manage to on-sell our townhouse before it settled. We didn’t make any money on it, but we didn’t lose money either.

What we did lose was that four years of opportunity.

We could have purchased a far better, established asset and enjoyed the growth that it would have delivered in that time.

What Off-the-Plan Buyers Often Overlook

When purchasers buy off the plan, they are not buying a finished product. They are buying a promise. That promise may take two, three, or even five years to materialise. During that time, market conditions can change dramatically. As can personal circumstances like mine. I didn’t anticipate that the project would take four years to complete.

Interest rates can rise. Lending policies can tighten. And in such climates, values can soften. Personal circumstances shift. What once felt affordable or strategic can quickly become a financial strain.

Many buyers assume that if circumstances change, they can simply sell the property before settlement. In theory, that sounds reasonable. In practice, developers often ensure that this option is either heavily restricted or commercially unviable.

Developer Control Is Often Built Into the Contract

Off-the-plan contracts are written by the developer’s legal team, for the developer’s benefit. Buried within the special conditions are clauses that give the developer extraordinary control over resale activity before settlement.

Common mechanisms include:

- Nomination restrictions, requiring developer consent before a buyer can nominate another purchaser to take over the contract prior to settlement

- Marketing controls, preventing advertising or resale at prices below the developer’s current stock

- Specific sales teams assigned to an onsell, meaning a buyer is bound to sell through the developer’s preferred sales agent.

These clauses are not accidental. Developers are protecting their price integrity and sales strategy. A distressed resale at a lower price can undermine the valuation of remaining stock and jeopardise their funding arrangements.

The Valuation Trap

This is where many buyers are caught out.

Imagine a buyer signed a contract three years ago at a premium price during a hot market. Fast forward to settlement, and comparable sales suggest the property is now worth less than the contract price. This isn’t even factoring in the marketer’s margin on the sale, (typical sales commissions for off-the-plan sales range from 3% -6%). When lender’s valuation comes in short, the buyer is required to contribute additional equity or risk default. (Default means not completing the contract; typically caused by not having the funds to settle on time).

At this point, selling prior to settlement feels like the logical solution, particularly for a buyer who doesn’t have the luxury of available equity or funding. But the developer may refuse consent to an on-sale at a lower price, or impose conditions that make it impossible to execute in time.

The buyer is left with very few options, and none of them are comfortable.

Why “Just Sell It” Isn’t a Strategy

I often hear buyers say, “If it doesn’t suit us later, we’ll just sell it.”

That assumption is naive.

Without understanding the nomination clauses, consent requirements, and developer approval mechanisms, buyers can vastly overestimate their exit options.

This is especially risky for buyers relying on future capital growth.

Due Diligence Is Everything

Buying off the plan isn’t always a disaster, as my first purchase in Mordialloc demonstrates. But it demands a much higher level of scrutiny. I didn’t apply that scrutiny as a 21 year old, and I’d consider that I got lucky with that particular purchase. Things could have been far worse.

If a buyer is completely committed to buying off the plan, here are my tips:

- Engage a property-savvy legal representative before signing. Be prepared to challenge any nasty clauses, because sometimes they can be struck or changed.

- Fully understand nomination and resale restrictions

- Stress-test affordability if values or lending conditions change

- Be realistic about build timeframes and market cycles

- Canvas the established property market to determine if there are other viable options within the budget

A Final Word of Caution

Off-the-plan purchases are often sold on optimism and aspiration. But property decisions need to be grounded in risk management and realism.

When developers retain control pricing, timing, and resale, buyers must enter with their eyes wide open. When off-the-plan doesn’t go to plan, the consequences can be both financially and emotionally upsetting.

A number of reforms have been initiated in Victoria for off-the-plan contracts in recent years. As recently as 2019, changes to Sunset Clauses were adopted, restricting developers from rescinding (stopping) contracts once a certain date of expiry arrived. Bad behaviour included delaying project timelines in rising markets to opportunistically re-sell at higher prices to new buyers. While some legal reforms have dampened the risks for buyers, other significant risks still remain.

When it comes to property investment, control matters. And for off-the-plan buying, control rarely sits with the buyer.

Other resources: