Property Investor or Property Speculator?

There are multiple property investment strategies out there and while some Advisors have a preference for a specific strategy, there is no right or wrong answer, provided the investor achieves a suitable outcome.

The differences in strategies revolve around how the debt is treated. It is either retired passively, retired in measured increments, or it isn’t retired at all.

Some investors will plan a “buy and hold” strategy whereby their portfolio is carefully engineered in an effort to hold every property over the long term until the rents have risen to a level that overtakes the holding costs, eventuating in the investor’s debt balance being paid off organically by the tenant. This strategy generally requires a comfortable blend of growth and rental yield in order to allow the investor the right cashflow environment for their debt retirement plans.

Some investors will plan a “buy and hold” strategy whereby their portfolio is carefully engineered in an effort to hold every property over the long term until the rents have risen to a level that overtakes the holding costs, eventuating in the investor’s debt balance being paid off organically by the tenant. This strategy generally requires a comfortable blend of growth and rental yield in order to allow the investor the right cashflow environment for their debt retirement plans.

Others will target capital growth properties with the view to crystallise some gains with the eventual sale of one or more star-performers and pay down the debts on the remaining assets with the profits from the sale. The obvious negative element to this strategy relates to taxes and fees (Capital Gains Tax, selling costs), but the significant blocker to the Capital Growth model is that borrowing constraints can hamper any investor’s ideal if they are unable to demonstrate to the lender that they have the debt servicing power. Particularly in today’s lending climate, an aggressive capital growth strategy could leave a few investors feeling hamstrung right now.

The idea of not retiring the debt may not rest so comfortably for some, but well known successful investors have established a strategy for themselves that will see them leave this earth with debt still outstanding. They have an approach that sees them borrowing equity from their successful capital growth gains whilst leaving the loans in place for the entirety of the life of their estate. While in theory it sounds interesting, lenders aren’t so easy to obtain “cash outs” from for no particular purpose, particularly if the individual is not drawing a traditional income. It will work for some pending their financial position but it’s not an available option for the mainstream.

So on that note, what do these three approaches have in common?

They rely on the investor holding the property for the longer term.

I meet prospective and real investors on a daily basis who have quite a different approach. They may be intent on adding value and “flipping”, renovating and subdividing for an imminent sale, or they may be keen to understand the next hotspot.

It can work for these approaches but I wouldn’t use the word investor for them. Rather, I’d suggest that they are either renovators, builders, developers or speculators.

Speculation introduces higher risk because the attempt to crystallise a short term gain is contingent on the asset’s growth based on a factor (or combination of factors) that apply to that asset outside of the general market.

Sourced from WIkipedia

There will always be regions and suburbs that demonstrate heady growth in a short space of time, but the questions that property speculators should ask themselves before buying are:

- Are the growth drivers genuine, sustainable and long term?

- Is the tenant-base strong and will vacancy rates remain tight?

- Will my financial position be OK if the town, project or region experiences a sharp downturn or doesn’t do what I’m speculating it could do?

From the Gold Coast to Gladstone, Bowen Basin to Broome, and many other-boom-and-bust locales, some investors fared well and others not so well.

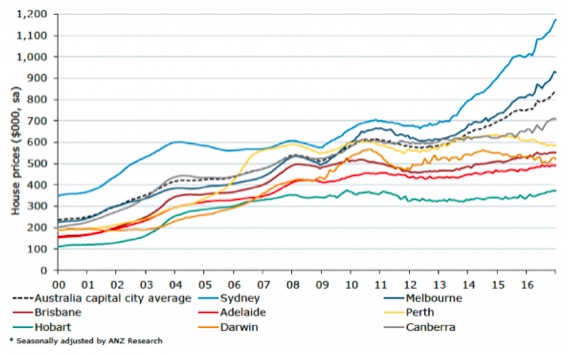

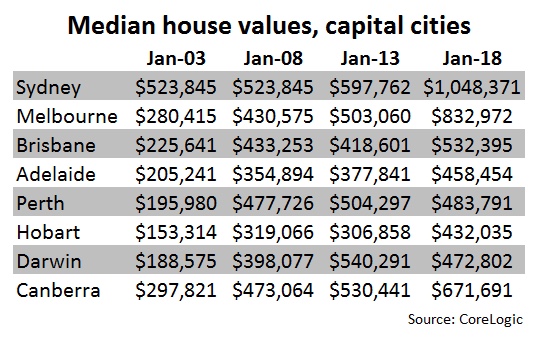

But when we focus on major capital cities, the long term median house price chart tells are far more stable story.

The saying, “it’s not timing the market, but time in the market” is perfectly illustrated when we focus on the long term growth in our capital city markets. Even a timeframe of 15 years as shown in the CoreLogic charts below has rewarded the investors who have held property assets since 2003 in Australian capitals. Despite the differential in capital growth rates across the cities (and a couple of shorter-term downturns), the long term ‘hold strategy’ certainly demonstrates the benefit of remaining resilient to the price movements at a micro level.

When I have a past client asking me whether they should sell a property they have held for less than five years to crystallise their gain, I feel a sense of disappointment that they have entered the market, paid stamp duty, sat still for what can only be described as an unfair amount of time, only to take a gain that could have been so much more had they been patient and plotted their investment course over the longer term.

If the strategy was Buy and Hold and their personal financial circumstances aren’t dictating the need to sell, I wonder how they’ll feel in ten years when they see what the same dwelling is worth.

Expecting a property to make you a strong gain in a short space of time is unfair.

A good industry friend was telling me back in 2009 about the gains he made when he sold multiple properties in Thornbury during the preceding decade. Even factoring in his taxes and fees, his profits were considerable.

Back then his median dwelling value in Thornbury was around $100,000. It now sits just shy of $1.2M.

His financial picture could have been quite different if he’d held them…. or even just one of them.

The power of time is one of a successful property investor’s most crucial ingredients.