The Federal Budget and its Uneven Impact Across Property Segments

On Tuesday 12th of May, at 7.30pm, our Federal Treasurer announced some significant tax change proposals. Two in particular, negative gearing and capital gains tax, will have an impact on our property markets.

Last week, I wrote a blog about both of these tax arrangements.

The proposed changes are significant. And they will absolutely skew markets.

Today I will cover what the impact of the negative gearing changes could mean for our markets. I won’t touch on the impact to renters in this blog, although I do believe the rental market will be negatively impacted.

For any investment property purchases after 7.30pm on 12th May 2026, negative gearing will no longer be able to be claimed against income for established property from 1st July, 2027.

What this will mean for those who either held investment property, (or held an executed contract for the purchase of investment property at 7.30pm om 12th May 2026), is that their negative gearing benefit is locked in. It will be grandfathered.

For those aspirational investors who planned to purchase an investment property in the future, the negative gearing benefit will no longer be claimable against their income. Instead, all ‘losses’ can be carried forward and claimed against property income, (either rental income or profits from sale proceeds).

The losses can be carried, year after year, for as long as it takes for the property rents to rise, and for the property to become cashflow-positive. For some who are already sitting on cashflow positive portfolios, negative gearing benefits will still be available for them under the new regime.

However, the injustice is stark for new investors. The negative cashflow required to hold a newly purchased, high capital growth asset is high. Previously, negative gearing aided the burden. Lenders factored the negative gearing benefit into their servicing calculators, and borrowers of investment properties had higher borrowing capacities as a result of this calculation. Now… banks will adjust their servicing calculators to compensate for the loss of this negative gearing benefit. Investors will borrow even less when they elect to buy established property.

Those who decide to purchase brand new property will reap the benefit of the negative gearing cashflow assistance. They will also qualify for higher borrowing capacity than their established property investor counterparts.

We all know what higher borrowing capacity does to markets. We saw it during COVID when interest rates dropped to 2%. The market took off in every city, in every state.

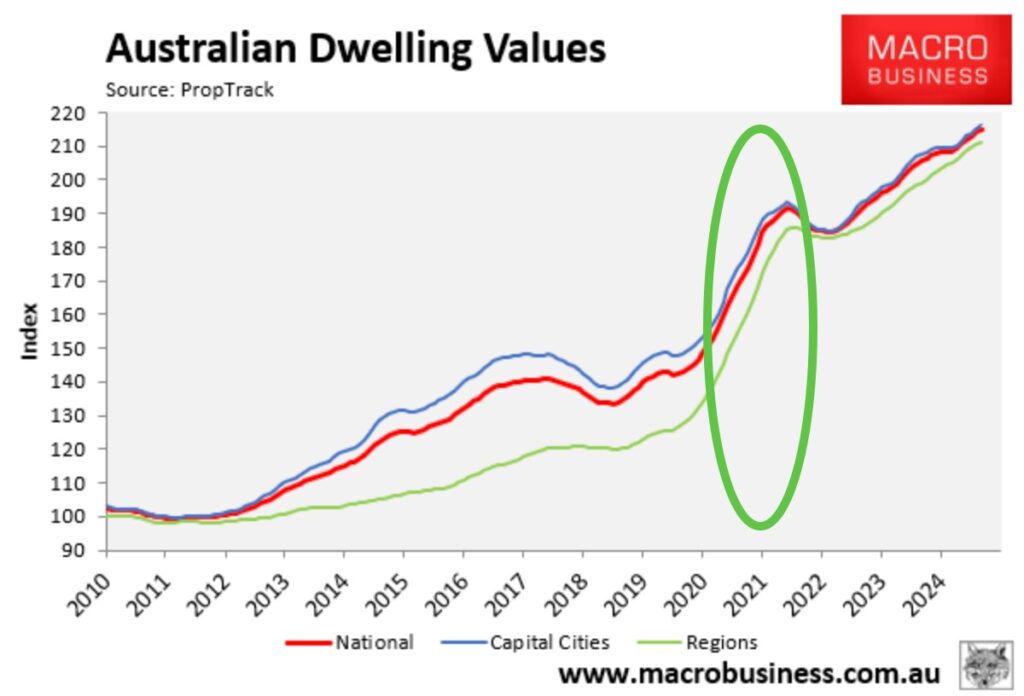

It’s obvious that many property investors will switch their preference from established property to new builds. They will be competing against first homebuyers in this space, as shown below in this chart. (Source: PropTrack, 21 November 2024, Vivien Topalovic).

First homebuyers are incentivised with grants, concessions, smaller initial deposits, and duties when they purchase brand new.

Now, first homebuyers in this space will be competing heavily with investors.

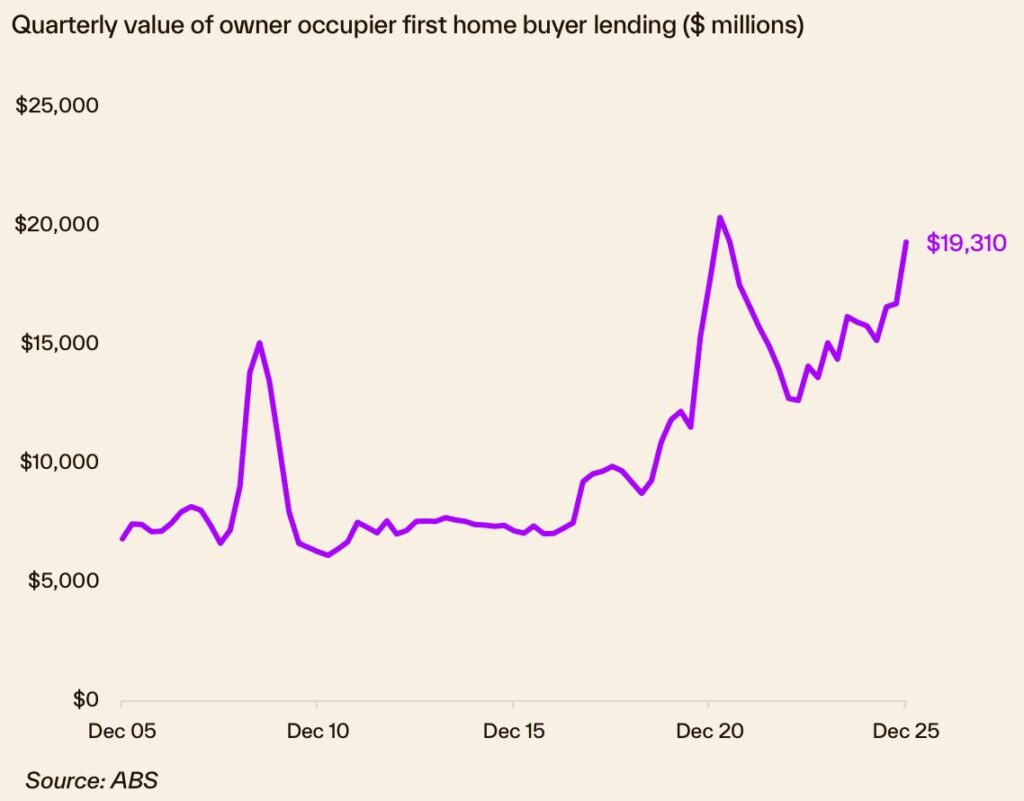

First home buyer activity has been strengthened with the government’s 5% deposit guarantee over the past year, and this is currently showing no signs of abating. Whether first homebuyers pivot to established housing is yet to be seen, but clearly first home buyers are one of the winners in this year’s budget, (alongside existing investors whose tax benefits are grandfathered).

“First home buyer lending was up sharply in Q4, increasing 6.8% by volume and 15.5% by value, coinciding with the expansion of the 5% deposit guarantee. First home buyers as a share of the value of home lending rose to 29.6% over the quarter, slightly above the decade average of 27.4%.” (Cotality Market Chart Pack May 2026).

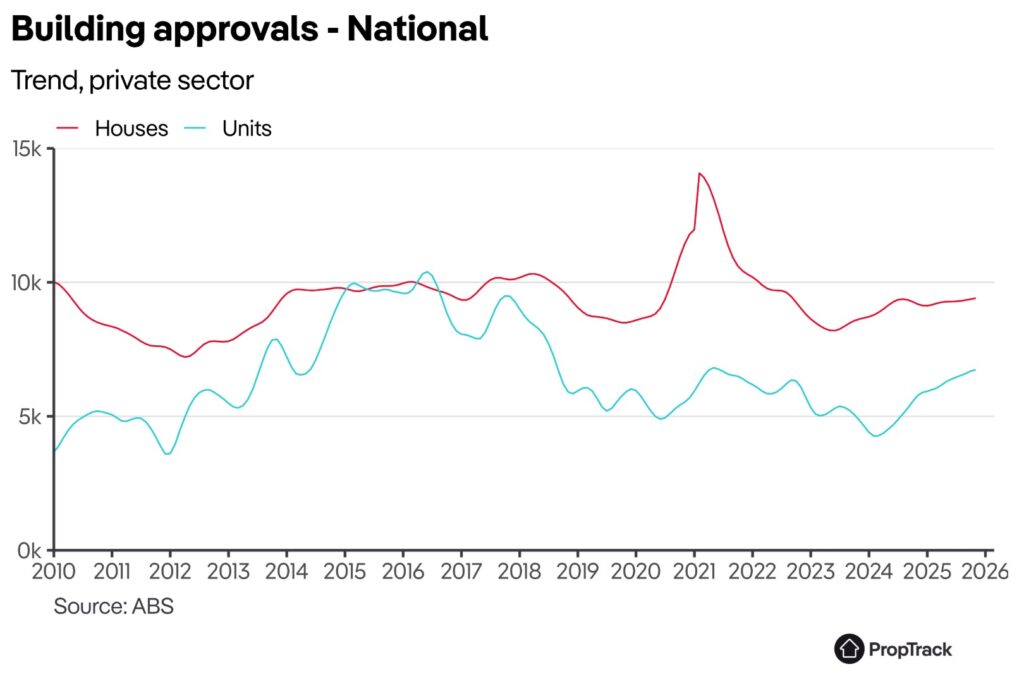

And while new building approvals have certainly increased over the past year, (shown below), the relative shortfall is still problematic. Our building approvals are falling short of our Housing Accord targets, and the proposed tax changes are going to put serious additional pressure on demand for new builds.

“While this is all good news, we are still well behind the pace of building we need to hit the National Cabinet target of 1.2 million homes over five years.” (28/1/26 PropTrack).

The chart also shows the increase is far sharper for units, than houses. Which leads me to my next point.

Houses are in high demand and this segment is relatively undersupplied when contrasted against units.

The media has highlighted the ‘enormous injustice’ for aspiring buyers, versus their Generation Boomer and Gen X counterparts this week. There has been a lot of discussion around the value of investing in the family home too. The main residence exemption remains untouched from capital gains tax regime changes, and we can anticipate many Australians opting to store their wealth in this vehicle.

What this will mean for our market will be interesting. Plenty of family home purchasers will likely focus their spend on higher priced options, as opposed to provisioning resources for investment property purchases. Some will value-add to their own homes, and it’s likely that housing turnover will reduce as people hold tight to their family homes.

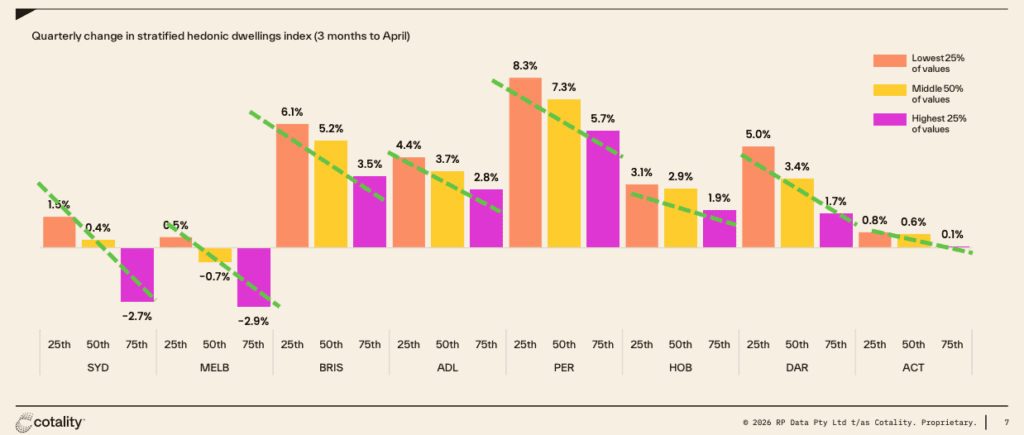

With reduced supply and increased demand, our higher priced property quartiles could see stronger growth. This will be a reversal from recent patterns where lower priced houses were experiencing the strongest growth; fuelled by investor demand and first homebuyer incentives.

While I am certain we’ll see strong growth in the new build markets, I caution investors who are adopting this strategy. The value of the property hinges strongly on it’s tax benefits. The inherent value of this only exists in the asset when it is initially purchased.

Like a collector’s toy in a sealed case, once the case is opened, the resale value of the toy is significantly reduced.

Those buying brand new need to understand value, and avoid overpaying in a heated market. This is particularly if a future government considers repealing (or modifying) the proposed tax changes. We cannot forget the lessons from forty years ago, when the last time a labour government removed negative gearing and then promptly reinstated it.

Now, more than ever before, investors need to think about the fundamental growth drivers that deliver long term property performance.

One of the most valuable ingredients is owner-occupier appeal.

As long as owner-occupiers are not subjected to property tax incentives and disincentives, they will select property based on genuine need and appeal.

Investors who do the same will benefit over the decades.