What is Negative Gearing?

This concept confuses so many, yet it shouldn’t be confusing. Perhaps we over-complicate it, or perhaps we associate it with detailed tax calculations. Whatever the reason, it isn’t complex and below will describe it in clear, simple terms.

Gearing is a word that refers to the ratio of borrowings to owners’ equity in a business venture. When borrowings are high relative to the owners stake in a business the situation is often referred to as ‘highly geared’ or leveraged. The level of gearing or borrowings impacts the cashflows of the business through loan payments made up of interest and loan principal.

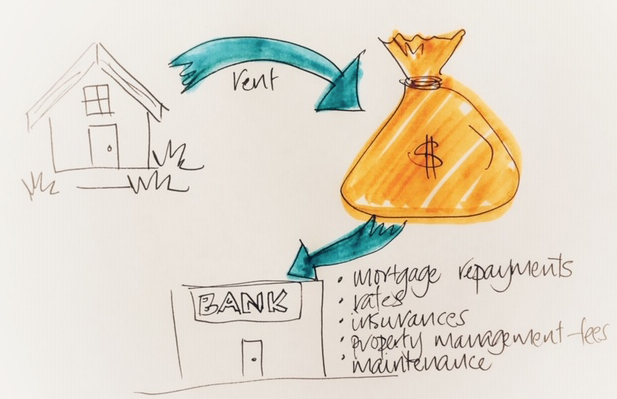

Investing in property can be regarded as a business activity. Imagine, as a landlord, that you are operating a business.

You are in the business of providing shelter.

You have some capital of your own to put towards your business, (ie. deposit), and you have a third party funder, (ie. a bank) who loans you the money to buy the asset, (ie. the property).

Your cost of running your business includes a combination of outgoings;

- the interest component of mortgage repayments,

- rates and taxes (ie. council rates, water rates, duties, land tax etc),

- insurances,

- property management fees, and

- maintenance costs.

Your income is your rent.

When the rental income received exceeds the running cost of your business, you will make a profit. In other words, your gross income position will be positive.

This business model is positively-geared.

You will be required to pay tax on this additional income that you are earning.

There are many properties within Australia that can provide the business owner with a gross-positive income. We will discuss them further on.

What happens when the rental income doesn’t adequately cover the running costs of the business though?

In this situation, the business model is negatively-geared.

This sketch demonstrates the cashflow, ie. the flow of the money before any tax benefit is applied. The business model is either operating with a positive gross cashflow, a neutral gross cashflow, or a negative gross cashflow.

So why would anyone want a negatively-geared business model?

They are losing money, yes?

Absolutely. They are operating at a loss. However, our tax system in Australia recognises the need for shelter and our government does not provide the required amount of shelter for the recipients who require it.

Our system currently relies on property investors to help provide shelter.

Our tax system assists property investors to provide shelter by crediting them with a tax rebate when the investor can demonstrate that their property has incurred an overall cash shortfall or loss. So when the investment is negatively geared as described above, the cash shortfall is cushioned by the return of some of the taxes already paid by the investor.

This cash cushion appears as a tax refund at the end of the financial year.

A basic way to consider this is as follows:

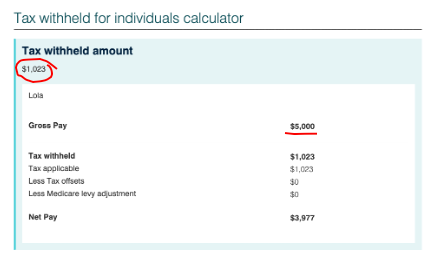

Lola earns $60,000 per year in her salaried job. Her gross monthly income is $5,000.

Lola’s tax witheld by her employer each month is $1,023 and this is credited by her employer to the ATO.

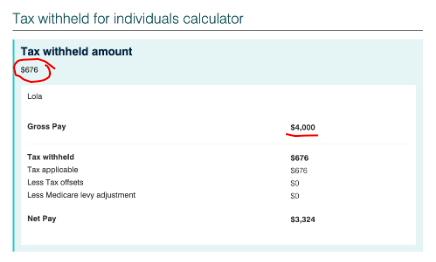

Lola owns an investment property and the losses she incurs are $1,000 per month. Lola’s effective total gross income as a result of running her investment property business is $48,000.

But Lola has already paid her tax for a full year based on earning $60,000.

When Lola completes her tax return, her tax payable is recalculated taking into account her losses from her investment property business.

The tax payable on $48,000 is $676 per month. The ATO credits Lola her effective tax overpayment in the form of a tax refund. In this (very simplified) instance, Lola’s tax refund is the differential over the full twelve months of the tax she paid, versus the tax she should have paid.

= 12 x ($1,023 – $676)

= $4,164

Lola will receive a tax refund in the form of a credit or a cheque.

When investors and accountants talk about “saving tax” or “getting tax back”, they are essentially talking about making a loss in order to claim SOME of it back.

There is no sense in this unless there is a bigger benefit long term.

So what is this benefit?

There is no point in buying a negatively geared property unless it is delivering something beyond a partial rebate on losses. The sole reason why a clever investor would purchase a negatively geared investment property, (outside of an altruistic motivation) is for capital growth.

When selected well, a negatively geared property will demonstrate strong returns, well beyond the rental income. Over the long term, the magnitude of the value growth of the asset will significantly eclipse the net losses incurred by the investor.

In addition, as rents increase over the longer term, the property will one day become positively-geared. The investor will then be required to pay tax on their positively changed income.

What a great problem to have. A property that exhibits value growth and a positive income stream.

Links:

https://www.commbank.com.au/articles/property/what-is-negative-gearing.html

https://treasury.gov.au/review/tax-white-paper/negative-gearing