Why 2021 will spell the return of investors

Back in 2014 our prudential regulator initiated some directives to our banks after concerns about the rising potential for a property bubble in Australia. Household debt had increased and investor numbers were troubling our reserve bank and regulator.

The banks were given a new set of targets, including a cap on new investor lending and an overall reduction of interest only lending.

Our regulator wanted to see household debt reduction. And they wanted it to happen quickly.

Our banks adopted the directive and through a series of changes to their investor lending policies, their actions caused a relatively rapid response. Some of the changes included;

- A differential between interest rates for owner-occupier and investor

- A heightened surcharge for interest only loans,

- Tougher servicing rates, ie. the interest rate at which the loan (and other existing loans) are assessed,

- Reduced LVRs, (loan to value ratio),

- Total aggregate borrowing caps,

- The introduction of really tough assessment scrutiny on household and lifestyle spending, and

- A reduced appetite for borrowers with any complexity to their earnings, for example; expats, self-employed, non-PR holders, etc.

Those who had interest only investment lending at the time were more or less forced to switch to principle and interest repayments at the end of their interest only period, and for some the switch was hard. The differential in terms of net (and gross) cashflow would have proven difficult for many investors who were highly leveraged and carrying significant debt.

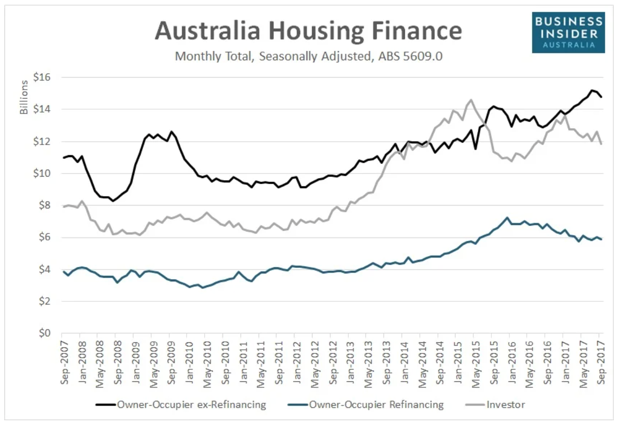

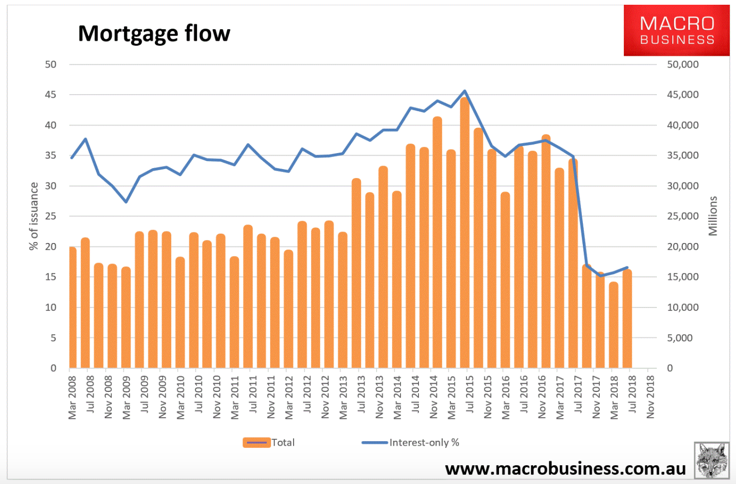

But over a four year period, the resultant lending statistics reflected APRA’s intended effect in terms of household debt, interest only lending and investor numbers as a percentage.

Source: MacroBusiness

According to David Llewellyn-Smith, Chief Strategist at the MB Fund and MB Super in 2018, “The total is now down from a peak of $583bn in March 2017 to $461bn five quarters later. Given banks have issued $95bn in new interest-only loans in that time we’ve seen as much as $200bn reset in outstanding interest-only loans already. The total refinancing task out to 2021 is roughly $450bn so the banks have gotten materially ahead of the curve. In short, so long as the economy keeps chugging along the task looks manageable. This is a great outcome for financial stability.”

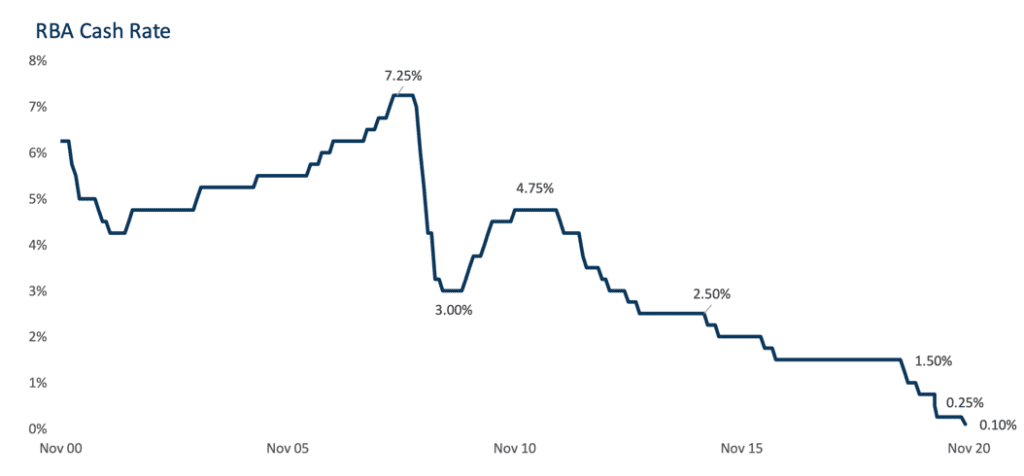

If we now wind the clock forward two years, nobody would have believed that our property market would sustain two downturns and (relatively quick) bounce-backs in this timeframe. In response to the difficult economic conditions, falling consumer sentiment and 2020’s first recession in nearly thirty years, our RBA lowered our interest rates to record lows.

Never before has money been so cheap in Australia.

Two powerful things have occurred in sync with the rate cuts.

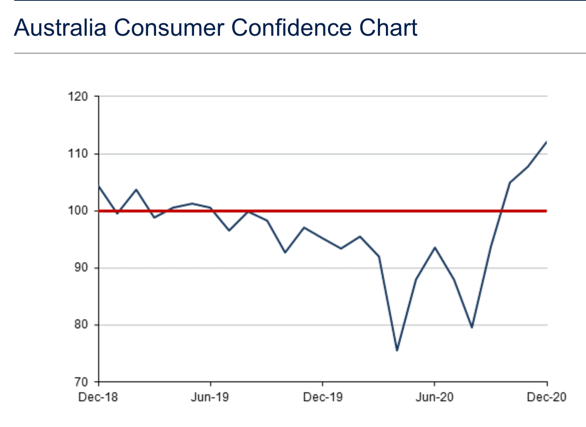

Firstly, consumer sentiment has bounced back into the positive. Whether it be confidence in the way our Federal Government handled economic stimulus during the onset of the pandemic, forced savings during COVID-19, or an appreciation of the resilience of the Australian property market, buyer and investor attitudes have changed dramatically since the low-point in April 2020.

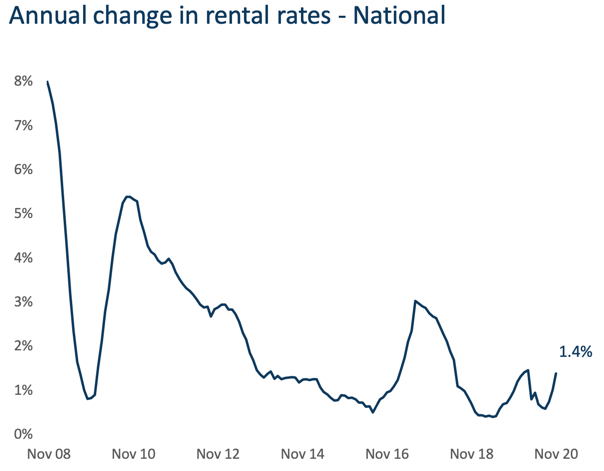

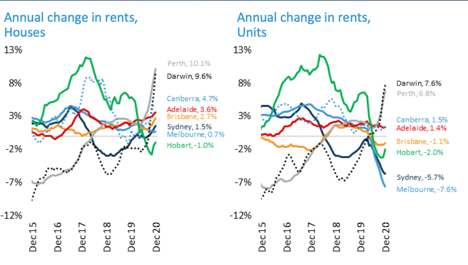

Secondly, rents have increased, (although not for all dwelling types across all markets). This is intriguing, indeed and it gives us insight into some of the dwelling types that skilled-up investors will and won’t target.

This CoreLogic chart clearly shows the uptick in rents across our national market.

Although not on its own, Melbourne’s line in each chart shines a light on the stark contrast between the unit and the housing market when it comes to changes in rent. Both Sydney and Melbourne have been significantly impacted by the COVID-19 freeze on new arrivals and in particular, overseas students, and Melbourne’s numbers are further exacerbated by an already-existing oversupply of high rise apartments in the CBD, Docklands and selected inner-ring locales.

Separating out this type of stock, the investor’s outlook is compelling.

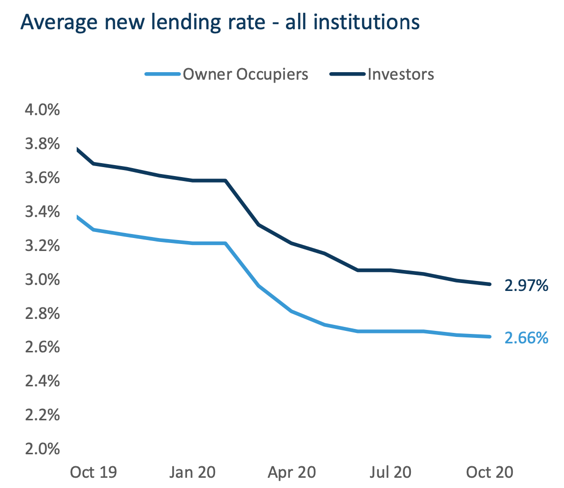

Negative gearing escaped the chopping block after our May 2019 Federal election result and not only are rental returns improving, but gross negative cashflow is lower as a direct result of the low interest rate environment we find ourselves in.

Even at a hiked level compared to P&I, the interest only offering has a significant impact on an investor’s cashflow. A recent, real-life example is telling. A client of ours who decided to access equity to purchase a $650,000 investment in Geelong faced two very different gross negative cashflow options while weighing up either an interest only loan vs a principle and interest loan by a monthly magnitude of greater than $500.

That’s a difference of more than $500 staying in his pocket each month.

The decision to pursue an interest only loan option vs a principle and interest loan is a very personal decision and we don’t encourage the reckless take up of debt, however we do endorse a carefully planned out approach which maximises the clients’ opportunity to built their wealth in line with their fiscal ability to do so. Debt retirement, (and the timing for this) must always be considered.

However, in contrast to the tight investor lending conditions from 2014-2018, 2021 appears to be heading in a different direction.

To further stimulate investor activity, the proposed changes to responsible lending in the coming months will likely ease the lender scrutiny and the previous restrictions on investment lending, (and in particular, interest-only lending options).

We believe that 2021 will spell the re-emergence of the investor.