The seven biggest investor mistakes in this climate

I’ve written many times over the years about common investor mistakes, but our economic and real estate climate has changed substantially since I’ve been a buyers agent. Some of the previous mistakes I’ve written about could be amplified these days. And some new risks have emerged.

Today’s blog samples the seven biggest mistakes many investors make in this era of property investing.

The first mistake starts with planning, or lack thereof. We have an abundance of tips and stories at our fingertips and the internet buzzes with hot ideas every minute of the day. However, sometimes a little bit of information can be dangerous, particularly when it falls into inexperienced hands. From PAYG tax variations to elaborate trusts, to rent-vesting, (to name just a few), buyers are often taking planning advice from those who are either not qualified to be giving such advice. (Or worse still, formulating a plan from generic internet information). Property planning takes into account so much more than just projected gains and borrowing capacity timelines. Proper planning involves medium and long-term goals, risk mitigation, tax benefits, and conservative buffers. Stage of life, future relationships, children, study and aging parents all form part of the list of considerations. All too often have I seen or heard sad stories about investors selling earlier than they intended because of planning oversights and poor assumptions.

The second mistake relates to chasing hotspots. Data only tells us so much, and often the hotspots featured on instagram are experiencing short term gains only, and some present other risks. A well-versed, genuinely data-centric buyer’s agent won’t give away their targeted areas to their competitors.

Algorithms also miss the granular detail, for example, street quality, floor plan feasibility (including cost-effective options for improvement), and local planning changes.

Targeting high tax benefits through high depreciating dwellings is the third mistake, and this error can set investor gains back significantly. Tax benefits via depreciation are maximised when the dwelling is brand new. The highest rate of depreciation occurs in the early years and slowly tapers off as the various building materials, fixtures and appliances age.

The issue with depreciation is that it essentially means an item is losing value.

If the rate of depreciation of the dwelling exceeds the rate of appreciation of the land, the property will lose value.

There is little point in losing a dollar to claim back the portion in the form of a tax refund, (at a maximum of 47 cents per ‘lost’ dollar, pending the investor’s income tax rate).

Often tax accountants will suggest to a client that they need to buy a property in order to utilise their tax deduction ability, but if they only knew that most brand new properties lose value, they’d likely suggest their client buys established, quality property and rely on the negative gearing benefit, along with a more modest depreciation benefit.

Not understanding new tenancy laws and minimum rental requirements is a more recent threat to the success of an investment in Victoria. Our rental laws have tightened substantially and our minimum rental standards are onerous, (and often expensive). To the untrained eye, a property may appear rent-ready, but once mandated appliance checks, gas and electricity compliance certificates, heating, cooling, window locks, blinds and cord tags, ovens, cooktops and safety are all taken into account, the cost can skyrocket. In particular, findings in the gas and electrical compliance checks can be major contributors to price blowouts. If an investor purchases a property with an older-style kitchen, for example, an oven with a limited space between the cooktop and the rangehood may not fulfil the rental minimum requirement for a 60cm gap (minimum). This often requires a complete kitchen realignment and can spell tens of thousands of dollars if the kitchen needs to be totally remodelled. Asbestos is another hidden risk, as is mould. These safety issues not only pose a threat to a renter’s safety, but can leave a new landlord with a depleted bank balance.

Aside from the physical considerations, legal changes around tenant’s rights, (issuing a notice to vacate, selling the property, and obtaining access to the property) also need to be well-understood.

Many landlords in Victoria don’t realise that they cannot lease their property for six months if they have previously issued a notice to vacate for the purposes of selling. In other words, if the sales campaign doesn’t eventuate with a sale, they will be faced with owning a vacant property for half a year before they are permitted to let the property again. While this legislative change has been created to deter landlords from finding loopholes to exit a tenant, it creates a financial issue (as well as a vacancy risk such as attracting crime and squatters) when a landlord has a genuine reason to withdraw their property from sale.

The fifth mistake is failing to provision for serious renovations when adopting a long term strategy. Most landlords think about the earliest updates when they initially purchase the property, but they neglect to plan ahead for more significant renovations. Kitchens and bathrooms often have a suitable lifespan of around 20-25 years for a rented property. Things start to fail and/or age, and many tenants are tougher with their wear and tear than a homeowner. Factoring in a kitchen and bathroom renovation every 20-25 years is a common calculation for an experienced, long term landlord. This equates to around $50,000 in today’s dollars for a new kitchen and bathroom, or several thousand dollars every 10-15 years for maintenance and upgrades. The cost is amplified when the property is interstate, because project coordination and management often exceeds a capable property manager’s mandate.

Formulating a brief based on future personal use is mistake number six. I’ve made this mistake once myself, and the cost-benefit equation should have been considered before I let my emotions and future plans take grip of the strategy. Property investment should be a pragmatic decision. An investor’s returns will be optimised when they can make an independent purchase decision which takes into account the growth drivers and desired yield Often, I meet purchasers who let their future plans and options override an optimal decision. Some of these future plans include post-retirement homes, units for children to use during university years, holiday homes, future assets to gift their children. The problem with this approach is that the investment strategy is undermined when personal needs compromise optimal growth options.

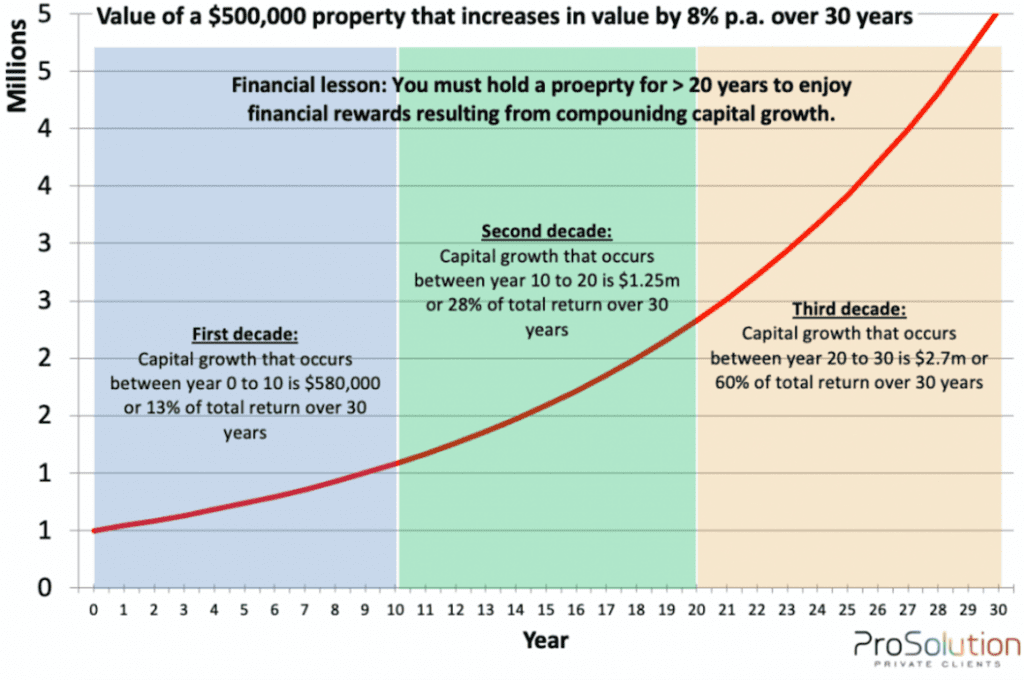

Thinking short term limits the property investor from achieving strong growth. Property is not a short-term, or trading asset. The entry and exit costs are large compared to other asset classes. Stamp duty, agent’s selling fees, marketing costs, and capital gains tax are all serious costs that will erode profits quickly. As Stuart Wemyss from ProSolution illustrated with a great chart (below), the largest gains on a buy-and-hold strategy are in the latter decades, not the first one.

For those investors who prefer fast gains, we suggest alternative asset classes. But it is important to note that risk and return go hand in hand.

Investing is often complex, but being mindful of these seven mistakes will help a committed property investor stay focused and optimise their returns.